How to create a financial forecast for a mortgage brokerage firm?

Developing and maintaining an up-to-date financial forecast for your mortgage brokerage firm is key in order to maintain visibility on your business’s future cash flows.

If you feel overwhelmed at the thought of putting together a mortgage brokerage firm financial forecast then don’t worry as this guide is here to help you.

We'll cover everything from: the main objectives of a financial forecast, the data you need to gather before starting, to the tables that compose it, and the tools that will help you create and maintain your forecast efficiently.

Let's get started!

Why create and maintain a financial forecast for a mortgage brokerage firm?

Creating and maintaining an up-to-date financial forecast is the only way to steer the development of your mortgage brokerage firm and ensure that it can be financially viable in the years to come.

A financial plan for a mortgage brokerage firm enables you to look at your business in detail - from income to operating costs and investments - to evaluate its expected profitability and future cash flows.

This gives you the visibility needed to plan future investments and expansion with confidence.

And, when your trading environment gets tougher, having an up to date mortgage brokerage firm forecast enables you to detect potential upcoming financing shortfalls in advance, enabling you to make adjustments or secure financing before you run out of cash.

It’s also important to remember that your mortgage brokerage firm's financial forecast will be essential when looking for financing. You can be 100% certain that banks and investors will ask to see your numbers, so make sure they’re set out accurately and attractively.

Need a convincing business plan?

The Business Plan Shop makes it easy to create a financial forecast to assess the potential profitability of your projects, and write a business plan that’ll wow investors.

What information is needed to build a mortgage brokerage firm financial forecast?

The quality of your inputs is key when it comes to financial modelling: no matter how good the model is, if your inputs are off, so will the forecast.

If you are building a financial plan to start a mortgage brokerage firm, you will need to have done your market research and have a clear picture of your sales and marketing strategies so that you can project revenues with confidence.

You will also need to have a clear idea of what resources will be required to operate the mortgage brokerage firm on a daily basis, and to have done your research with regard to the equipment needed to launch your venture (see further down this guide).

If you are creating a financial forecast of an existing mortgage brokerage firm, things are usually simpler as you will be able to use your historical accounting data as a budgeting base, and complement that with your team’s view on what lies ahead for the years to come.

Let's now zoom in on what will go in your mortgage brokerage firm's financial forecast.

The sales forecast for a mortgage brokerage firm

From experience, it is usually best to start creating your mortgage brokerage firm financial forecast by your sales forecast.

To create an accurate sales forecast for your mortgage brokerage firm, you will have to rely on the data collected in your market research, or if you're running an existing mortgage brokerage firm, the historical data of the business, to estimate two key variables:

- The average price

- The number of monthly transactions

To get there, you will need to consider the following factors:

- Changes in interest rates: Fluctuations in interest rates can greatly impact the average price of mortgages and the number of monthly transactions. When interest rates are low, more clients may be interested in taking out mortgages, resulting in higher transaction numbers and possibly lower average prices. However, when interest rates are high, fewer clients may be able to afford mortgages, leading to lower transaction numbers and potentially higher average prices.

- Housing market conditions: The state of the housing market can also affect the average price and number of monthly transactions for a mortgage brokerage firm. In a seller's market, where there is high demand for housing and low supply, mortgage prices may increase due to competition among buyers. This could result in a higher average price for the brokerage firm. On the other hand, in a buyer's market, where there is low demand for housing and high supply, mortgage prices may decrease, resulting in a lower average price for the firm. The number of transactions may also be impacted, as more clients may be looking to buy in a seller's market compared to a buyer's market.

- Government policies and regulations: Changes in government policies and regulations can also affect the mortgage market and, in turn, the average price and number of monthly transactions for a brokerage firm. For example, if the government introduces new regulations that make it more difficult for clients to qualify for mortgages, this could result in a decrease in the number of monthly transactions and potentially an increase in average prices as the firm may need to work with more qualified clients.

- Economic conditions: Overall economic conditions can also play a role in the average price and number of monthly transactions for a brokerage firm. During an economic downturn, clients may be more cautious about taking on large financial commitments, such as mortgages, resulting in lower transaction numbers and potentially higher average prices. In contrast, during a robust economy, clients may be more confident in their financial stability and more willing to take on mortgages, leading to higher transaction numbers and potentially lower average prices.

- Competition: The level of competition in the mortgage brokerage industry can also affect the average price and number of monthly transactions for a firm. If there are many other brokerage firms in the market, this could drive prices down as clients have more options to choose from. On the other hand, if there are fewer competitors, a firm may be able to charge higher prices and potentially see an increase in transaction numbers as clients may have fewer alternatives.

Once you have an idea of what your future sales will look like, it will be time to work on your overhead budget. Let’s see what this entails.

Need a convincing business plan?

The Business Plan Shop makes it easy to create a financial forecast to assess the potential profitability of your projects, and write a business plan that’ll wow investors.

The operating expenses for a mortgage brokerage firm

The next step is to estimate the costs you’ll have to incur to operate your mortgage brokerage firm.

These will vary based on where your business is located, and its overall size (level of sales, personnel, etc.).

But your mortgage brokerage firm's operating expenses should normally include the following items:

- Staff costs: This includes salaries, bonuses, and benefits for all employees, including loan officers, underwriters, and administrative staff.

- Accountancy fees: As a mortgage brokerage firm, you will need to hire an accountant to handle your financial statements, tax filings, and other financial matters.

- Insurance costs: You will need various types of insurance to protect your business, such as professional liability insurance, general liability insurance, and property insurance.

- Software licenses: To operate efficiently, you will need to invest in software for loan processing, customer relationship management, and accounting.

- Banking fees: As a mortgage brokerage firm, you will have to pay fees for bank accounts, wire transfers, and other banking services.

- Marketing and advertising: To attract clients, you will need to invest in marketing and advertising efforts, such as online ads, flyers, and partnerships with real estate agents.

- Office rent and utilities: This includes the cost of renting office space, as well as expenses for utilities like electricity, water, and internet.

- Professional development: To stay competitive, you will need to invest in ongoing training and education for your staff.

- Legal fees: You may need to seek legal advice for contracts, compliance issues, and other legal matters.

- Travel expenses: As a mortgage brokerage firm, you may need to travel for meetings with clients or industry events.

- Office supplies and equipment: This includes the cost of purchasing and maintaining office equipment, such as computers, printers, and furniture.

- Telephone and internet: You will need reliable telephone and internet services to communicate with clients and conduct business.

- Professional memberships and subscriptions: You may need to join professional organizations and subscribe to industry publications for networking and staying updated on industry trends.

- Commissions and fees: As a mortgage brokerage firm, you will need to pay commissions and fees to lenders, appraisers, and other professionals involved in the loan process.

- Office maintenance and cleaning: This includes the cost of keeping your office clean and well-maintained for a professional appearance.

This list is not exhaustive by any means, and will need to be tailored to your mortgage brokerage firm's specific circumstances.

What investments are needed to start or grow a mortgage brokerage firm?

Once you have an idea of how much sales you could achieve and what it will cost to run your mortgage brokerage firm, it is time to look into the equipment required to launch or expand the activity.

For a mortgage brokerage firm, capital expenditures and initial working capital items could include:

- Office Space: As a mortgage brokerage firm, you'll need a professional office space to conduct your business. This could include renting or purchasing a commercial property, office furniture, and equipment such as computers, printers, and phones.

- Software and Technology: In order to effectively manage your clients and their mortgage applications, you'll need to invest in software and technology. This could include loan origination software, customer relationship management (CRM) systems, and accounting software.

- Training and Licensing: As a mortgage brokerage firm, you'll need to ensure that your employees are properly trained and licensed to provide mortgage services. This may require investing in training programs, licensing exams, and continuing education courses.

- Marketing Materials: While marketing and advertising expenses may not be included in your expenditure forecast, the cost of creating marketing materials such as brochures, business cards, and website development should be considered as a capital expenditure.

- Security and Insurance: In order to protect your business and your clients' information, you may need to invest in security measures such as security cameras, alarm systems, and cybersecurity software. Additionally, you'll need to budget for insurance premiums to cover any potential risks or liabilities.

Again, this list will need to be adjusted according to the specificities of your mortgage brokerage firm.

Need a convincing business plan?

The Business Plan Shop makes it easy to create a financial forecast to assess the potential profitability of your projects, and write a business plan that’ll wow investors.

The financing plan of your mortgage brokerage firm

The next step in the creation of your financial forecast for your mortgage brokerage firm is to think about how you might finance your business.

You will have to assess how much capital will come from shareholders (equity) and how much can be secured through banks.

Bank loans will have to be modelled so that you can separate the interest expenses from the repayments of principal, and include all this data in your forecast.

Issuing share capital and obtaining a bank loan are two of the most common ways that entrepreneurs finance their businesses.

What tables compose the financial plan for a mortgage brokerage firm?

Now let's have a look at the main output tables of your mortgage brokerage firm's financial forecast.

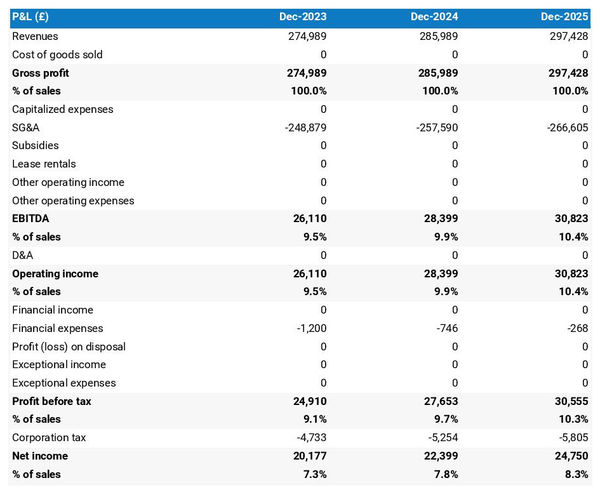

The projected profit & loss statement

The projected profit & loss shows how profitable your mortgage brokerage firm is likely to be in the years to come.

For your mortgage brokerage firm to be financially viable, your projected P&L should ideally show:

- Sales growing above inflation (the higher the better)

- Profit margins which are stable or expanding (the higher the better)

- A net profit at the end of each financial year (the higher the better)

This is for established mortgage brokerage firms, there is some leniency for startups which will have numbers that will look a bit different than existing businesses.

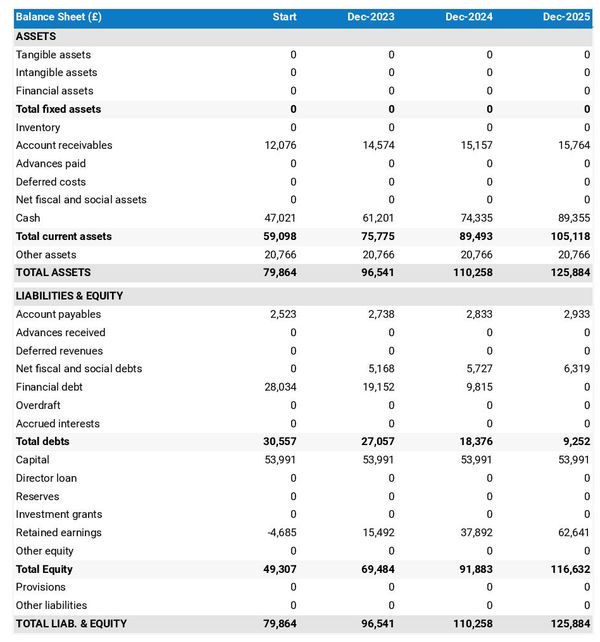

The projected balance sheet

Your mortgage brokerage firm's forecasted balance sheet enables you to assess your financial structure and working capital requirements.

It is composed of three types of elements: assets, liabilities and equity:

- Assets: represent what the business owns and uses to produce cash flows. It includes resources such as cash, equipment, and accounts receivable (money owed by clients).

- Liabilities: represent funds advanced to the business by lenders and other creditors. It includes items such as accounts payable (money owed to suppliers), taxes due and loans.

- Equity: is the combination of what has been invested by the business owners and the cumulative profits and losses generated by the business to date (which are called retained earnings). Equity is a proxy for the value of the owner's stake in the business.

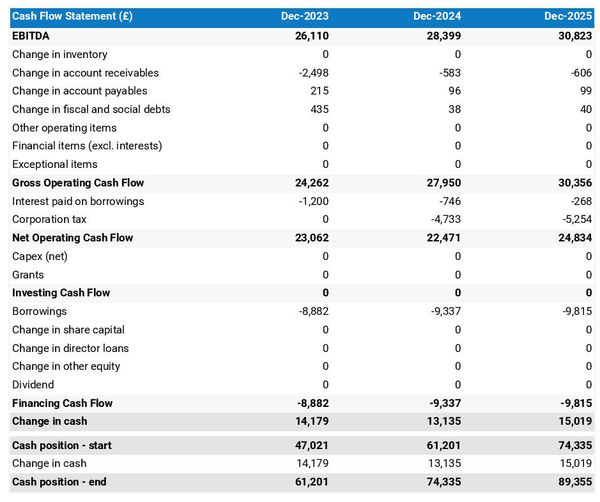

The projected cash flow statement

A projected cash flow statement for a mortgage brokerage firm is used to show how much cash the business is generating or consuming.

The cash flow forecast is usually organised by nature to show three key metrics:

- The operating cash flow: do the core business activities generate or consume cash?

- The investing cash flow: how much is the business investing in long-term assets (this is usually compared to the level of fixed assets on the balance sheet to assess whether the business is regularly maintaining and renewing its equipment)?

- The financing cash flow: is the business raising new financing or repaying financiers (debt repayment, dividends)?

Cash is king and keeping an eye on future cash flows is imperative for running a successful business. Therefore, you should pay close attention to your mortgage brokerage firm's cash flow forecast.

If you are trying to secure financing, note that it is customary to provide both yearly and monthly cash flow forecasts in a financial plan - so that the reader can analyze seasonal variation and ensure the mortgage brokerage firm is appropriately capitalised.

Need a convincing business plan?

The Business Plan Shop makes it easy to create a financial forecast to assess the potential profitability of your projects, and write a business plan that’ll wow investors.

Which tool should you use to create your mortgage brokerage firm's financial projections?

Building a mortgage brokerage firm financial forecast is not difficult provided that you use the right tool for the job. Let’s see what options are available below.

Using online financial forecasting software to build your mortgage brokerage firm's projections

The modern and easiest way is to use professional online financial forecasting software such as the one we offer at The Business Plan Shop.

There are several advantages to using specialised software:

- You can easily create your financial forecast by letting the software take care of the financial calculations for you without errors

- You have access to complete financial forecast templates

- You get a complete financial forecast ready to be sent to your bank or investors

- You can easily track your actual financial performance against your financial forecast, and recalibrate your forecast as the year goes by

- You can create scenarios to stress test your forecast's main assumptions

- You can easily update your forecast as time goes by to maintain visibility on future cash flows

- You have a friendly support team on standby to assist you when you are stuck

- It’s cost-efficient and much cheaper than using an accountant or consultant (see below)

If you are interested in this type of solution, you can try our forecasting software for free by signing up here.

Calling in a financial consultant or chartered accountant

Outsourcing the creation of your mortgage brokerage firm financial forecast is another possible solution.

This will cost more than using software as you can expect as your price will have to cover the accountant’s time, software cost, and profit margin.

Price can vary greatly based on the complexity of your business. For a small business, from experience, a simple three-year financial forecast (including a balance sheet, income statement, and cash flow statement) will start at around £700 or $1,000.

Bear in mind that this is for forecasts produced at a single point in time, updating or tracking your forecast against actuals will cost extra.

If you decide to outsource your forecasting:

- Make sure the professional has direct experience in your industry and is able to challenge your assumptions constructively.

- Steer away from consultants using sectorial ratios to build their client’s financial forecasts (these projections are worthless for a small business).

Why not use a spreadsheet such as Excel or Google Sheets to build your mortgage brokerage firm's financial forecast?

Creating an accurate and error-free mortgage brokerage firm financial forecast with a spreadsheet is very technical and requires a deep knowledge of accounting and an understanding of financial modelling.

Very few business owners are financially savvy enough to be able to build a forecast themselves on Excel without making mistakes.

Lenders and investors know this, which is why forecasts created on Excel by the business owner are often frowned upon.

Having numbers one can trust is key when it comes to financial forecasting and to that end using software is much safer.

Using financial forecasting software is also faster than using a spreadsheet, and, with the rise of artificial intelligence, software is also becoming smarter at helping us analyse the numbers to make smarter decisions.

Finally, like everything with spreadsheets, tracking actuals vs. forecasts and keeping your projections up to date as the year progresses is manual, tedious, and error-prone. Whereas financial projection software like The Business Plan Shop is built for this.

Need a convincing business plan?

The Business Plan Shop makes it easy to create a financial forecast to assess the potential profitability of your projects, and write a business plan that’ll wow investors.

Use our financial projection templates for inspiration

The Business Plan Shop has dozens of financial forecast templates available.

Our examples contain a complete business plan with a financial forecast and a written presentation of the company, the team, the strategy, and the medium-term objectives.

Whether you are just starting out or already have your own mortgage brokerage firm, looking at our financial forecast template is a good way to:

- Understand what a complete business plan should look like

- Understand how you should model financial items for your mortgage brokerage firm

Takeaways

- A financial projection shows expected growth, profitability, and cash generation for your business over the next three to five years.

- Tracking actuals vs. forecast and keeping your financial forecast up-to-date is the only way to maintain visibility on future cash flows.

- Using financial forecasting software makes it easy to create and maintain up-to-date projections for your mortgage brokerage firm.

You have reached the end of our guide. We hope you now have a better understanding of how to create a financial forecast for a mortgage brokerage firm. Don't hesitate to contact our team if you have any questions or want to share your experience building forecasts!

Need a convincing business plan?

The Business Plan Shop makes it easy to create a financial forecast to assess the potential profitability of your projects, and write a business plan that’ll wow investors.

Also on The Business Plan Shop

- Example of financial projections

- How to create a turnover forecast for a business?

- Sample financial forecast for business idea

Know someone who runs or wants to start a mortgage brokerage firm? Share our financial projection guide with them!

Founder & CEO at The Business Plan Shop Ltd