What is a Profit & Loss forecast and why is it important?

Have you been fine-tuning your business idea for months and now feel anxious about writing your business plan? Are you already anticipating the financial forecast part? Or maybe you're in the middle of writing it, but finding it a difficult feat? Either way, this article is here to help you!

Here, we'll review one of the financial statements of the forecast: the Profit & Loss budget. You will understand what the P&L really is, what it is used for, what it is made up of, what it enables you to evaluate, how to interpret it, and what its limits are.

You will also find a concrete example, explained in detail, and our unstoppable trick to create your financial forecast easily and without unnecessary stress. Simply follow the guide!

What is a Profit & Loss forecast and what is it used for?

The financial forecast, an essential part of a business plan, consists of three major elements:

- the P&L statement

- the balance sheet

- the cash flow statement

The P&L statement is therefore one of the financial statements within the business plan's financial forecast.

It shows the income generated by the company over one or more financial years, enabling you to quickly evaluate:

- the company's growth: i.e. the increase in its turnover

- its profitability: i.e. the ratio between the net income obtained and the revenue generated

- the cost structure of the latter: i.e. the total costs generated by the company's operations

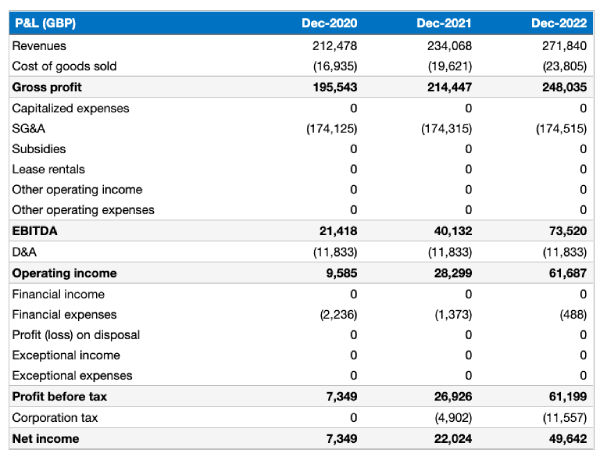

Example of a Profit & Loss forecast

Here's an example of a profit & loss forecast:

This table includes all the elements in the P&L, as well as the elements that will allow you to calculate them. For example, gross margin is calculated by subtracting the cost of goods sold from sales.

Definition of the categories of the P&L forecast:

- Revenues are the total amount of products and services sold over a reference accounting period. Excluding taxes such as GST in the US or VAT in the UK.

- Cost of goods sold (COGS) is the value of the products sold by the company.

- Gross profit represents the difference between the selling price and the cost of the product or service sold by the company.

- SG&A expenses include the company's administrative, commercial, and general expenses.

- Lease rentals are the total lease payments made by the company.

- EBITDA is the company's operating income before depreciation and amortization, interests and taxes. If it is positive, the company is profitable: it sells its products or services for more than they cost to manufacture. If it is negative, the company is experiencing serious operational difficulties.

- D&A (Depreciation & Amortization) is the accounting charge reflecting the loss of economic value of a fixed asset over time (i.e. wear and tear).

- Operating income or (EBIT) represents the operating income generated by the company through the normal operation of its production factors.

- Financial income is the financial income generated by the company (such as interests earned on saving accounts).

- Financial expenses include the interest on loans paid by the company. They, therefore, vary according to the company's level of indebtedness and the rates at which it has borrowed.

- The profit (or loss) on disposal corresponds to the gain (or loss) on the disposal, i.e. resale, of a fixed asset (land, premises, vehicles, etc.).

- Exceptional income and expenses include the results from non operating activities.

- Profit before tax is the profit or loss before corporation tax.

- Corporation tax is a tax levied by the State, calculated based on profits made by the company on state territory (it is a percentage of taxable profits).

- Net income is the difference recorded, over a given period of time, between all the income and expenses to which the company is subject. If the net result is positive, the company makes a profit.

Can your business idea be profitable?

Just enter your data and let The Business Plan Shop crunch the numbers. We will tell if your business idea can generate profits and cash flows, and how much you need to get started.

How can I interpret the Profit & Loss forecast?

Many ratios allow you to contextualize and interpret the company's profit and loss. We present the main ratios below, highlighting the fact that this list is not exhaustive and lists only the most frequently used ratios:

Revenue growth:

- Formula: (revenues in T/revenues in T-1) - 1

- Interpretation: it measures the company's ability to grow, acquire new customers or generate more revenue from existing customers.

Gross profit margin in % of revenues:

- Formula: gross profit/revenues

- Interpretation: it allows you to evaluate the commercial strategy of the company (the difference between the selling price and the purchase cost of the goods sold or the cost of the manufactured products).

EBITDA margin as a percentage of revenues:

- Formula: EBITDA/revenues

- Interpretation: it allows you to evaluate the operational profitability of the company

Interests coverage ratio:

- Formula: EBITDA/financial expenses

- Interpretation: it measures the company's ability to generate sufficient operating profitability to pay the interest on its debt.

Net debt to EBITDA:

- Formula: Net debt/EBITDA

- Interpretation: it allows a quick assessment of the company's ability to repay its financial debt using EBITDA as an approximation of cash flow.

Effective tax rate:

- Formula: Corporation tax/profit before tax

- Interpretation: it measures the weight of taxation for the company

Growth in overheads:

- Formula: (SG&A T/SG&A T-1) - 1

- Interpretation: it measures the company's ability to control its cost structure, to be compared with the evolution of turnover and EBITDA margin.

What are the limits of the P&L forecast?

The Profit and Loss forecast is a key element of the financial forecast. It enables the project owner to anticipate the financial aspects of his business and potential investors to evaluate the fundamental elements of business, which are its growth, profitability and cost structure.

However, the Profit & Loss forecast is just one tool among others and is far from being complete. It even has a major drawback: the P&L does not take into account the impact of working capital, and cash flows in general (purchase of fixed assets, loan repayments, etc.) which are in the cash flow statement.

It is therefore important to analyze all the elements of the financial forecast: including the projected balance sheet, and the projected cash flow statement.

Can your business idea be profitable?

Just enter your data and let The Business Plan Shop crunch the numbers. We will tell if your business idea can generate profits and cash flows, and how much you need to get started.

How to establish a Profit & Loss forecast?

To create a perfect profit and loss forecast, even if you are not familiar with this exercise and have no particular affinity with numbers, you can use online forecasting software.

This type of tool will enable you to create your financial forecast very easily: fill in the data according to the instructions of the software, which will take care of the calculations and accounting aspects for you.

You will even be able to create graphs that will simplify the reading of your financial forecast and facilitate its interpretation.

If you are interested in this type of tool, you can try our software for free here.

Need a convincing business plan?

The Business Plan Shop makes it easy to create a financial forecast and write a business plan to help convince investors that your business idea can be profitable.

Conclusion

The financial forecast (and the P&L in particular) are key elements of the business plan that are relatively difficult to create. It is, therefore, better to choose a tool that will help you to do the job easily.

After all, a financial forecast is nothing more than a mechanism to assess your company's profitability and find ways to improve it. We hope we've helped you understand what is a Profit & Loss forecast and why it's important !

Also on The Business Plan Shop

- How to do a financial forecast for a new business?

- Example of a financial forecast

- How to create a sales forecast for a business?

Founder & CEO at The Business Plan Shop Ltd