How to write a business plan for a mortgage broker?

Putting together a business plan for a mortgage broker can be daunting - especially if you're creating a business for the first time - but with this comprehensive guide, you'll have the necessary tools to do it confidently.

We will explore why writing one is so important in both starting up and growing an existing mortgage broker, as well as what should go into making an effective plan - from its structure to content - and what tools can be used to streamline the process and avoid errors.

Without further ado, let us begin!

Why write a business plan for a mortgage broker?

Being clear on the scope and goals of the document will make it easier to understand its structure and content. So before diving into the actual content of the plan, let's have a quick look at the main reasons why you would want to write a mortgage broker business plan in the first place.

To have a clear roadmap to grow the business

Small businesses rarely experience a constant and predictable environment. Economic cycles go up and down, while the business landscape is mutating constantly with new regulations, technologies, competitors, and consumer behaviours emerging when we least expect it.

In this dynamic context, it's essential to have a clear roadmap for your mortgage broker. Otherwise, you are navigating in the dark which is dangerous given that - as a business owner - your capital is at risk.

That's why crafting a well-thought-out business plan is crucial to ensure the long-term success and sustainability of your venture.

To create an effective business plan, you'll need to take a step-by-step approach. First, you'll have to assess your current position (if you're already in business), and then identify where you'd like your mortgage broker to be in the next three to five years.

Once you have a clear destination for your mortgage broker, you'll focus on three key areas:

- Resources: you'll determine the human, equipment, and capital resources needed to reach your goals successfully.

- Speed: you'll establish the optimal pace at which your business needs to grow if it is to meet its objectives within the desired timeframe.

- Risks: you'll identify and address potential risks you might encounter along the way.

By going through this process regularly, you'll be able to make informed decisions about resource allocation, paving the way for the long-term success of your business.

To maintain visibility on future cash flows

Businesses can go for years without making a profit, but they go bust as soon as they run out of cash. That's why "cash is king", and maintaining visibility on your mortgage broker's future cash flows is critical.

How do I do that? That's simple: you need an up-to-date financial forecast.

The good news is that your mortgage broker business plan already contains a financial forecast (more on that later in this guide), so all you have to do is to keep it up-to-date.

To do this, you need to regularly compare the actual financial performance of your business to what was planned in your financial forecast, and adjust the forecast based on the current trajectory of your business.

Monitoring your mortgage broker's financial health will enable you to identify potential financial problems (such as an unexpected cash shortfall) early and to put in place corrective measures. It will also allow you to detect and capitalize on potential growth opportunities (higher demand from a given segment of customers for example).

To secure financing

Whether you are a startup or an existing business, writing a detailed mortgage broker business plan is essential when seeking financing from banks or investors.

This makes sense given what we've just seen: financiers want to ensure you have a clear roadmap and visibility on your future cash flows.

Banks will use the information included in the plan to assess your borrowing capacity (how much debt your business can support) and your ability to repay the loan before deciding whether they will extend credit to your business and on what terms.

Similarly, investors will review your plan carefully to assess if their investment can generate an attractive return on investment.

To do so, they will be looking for evidence that your mortgage broker has the potential for healthy growth, profitability, and cash flow generation over time.

Now that you understand why it is important to create a business plan for a mortgage broker, let's take a look at what information is needed to create one.

Need a convincing business plan?

The Business Plan Shop makes it easy to create a financial forecast to assess the potential profitability of your projects, and write a business plan that’ll wow investors.

What information is needed to create a business plan for a mortgage broker?

Writing a mortgage broker business plan requires research so that you can project sales, investments and cost accurately in your financial forecast.

In this section, we cover three key pieces of information you should gather before drafting your business plan!

Carrying out market research for a mortgage broker

Before you begin writing your business plan for a mortgage broker, conducting market research is a critical step in ensuring precise and realistic financial projections.

Market research grants you valuable insights into your target customer base, competitors, pricing strategies, and other crucial factors that can impact the success of your business.

In the course of this research, you may stumble upon trends that could impact your mortgage broker.

Your mortgage broker may discover that potential customers are increasingly looking for fixed-rate mortgages. Additionally, they may find that there is a growing preference for digital mortgage services that provide a streamlined, convenient experience.

Such market trends play a pivotal role in revenue forecasting, as they provide essential data regarding potential customers' spending habits and preferences.

By integrating these findings into your financial projections, you can provide investors with more accurate information, enabling them to make well-informed decisions about investing in your mortgage broker.

Developing the sales and marketing plan for a mortgage broker

As you embark on creating your mortgage broker business plan, it is crucial to budget sales and marketing expenses beforehand.

A well-defined sales and marketing plan should include precise projections of the actions required to acquire and retain customers. It will also outline the necessary workforce to execute these initiatives and the budget required for promotions, advertising, and other marketing efforts.

This approach ensures that the appropriate amount of resources is allocated to these activities, aligning with the sales and growth objectives outlined in your business plan.

The staffing and equipment needs of a mortgage broker

As you embark on starting or expanding your mortgage broker, having a clear plan for recruitment and capital expenditures (investment in equipment and real estate) is essential for ensuring your business's success.

Both the recruitment and investment plans must align with the timing and level of growth projected in your forecast, and they require appropriate funding.

Staffing costs for a mortgage broker may include salary for the broker, loan officers, and administrative staff, as well as taxes and benefits associated with those salaries. Equipment costs may include computers and software, office furniture, and other equipment necessary to run the business.

To create a realistic financial forecast, you also need to consider other operating expenses associated with the day-to-day running of your business, such as insurance and bookkeeping.

With all the necessary information at hand, you are ready to begin crafting your business plan and developing your financial forecast.

What goes into your mortgage broker's financial forecast?

The financial forecast of your mortgage broker's business plan will enable you to assess the growth, profitability, funding requirements, and cash generation potential of your business in the coming years.

The four key outputs of a financial forecast for a mortgage broker are:

- The profit and loss (P&L) statement,

- The projected balance sheet,

- The cash flow forecast,

- And the sources and uses table.

Let's look at each of these in a bit more detail.

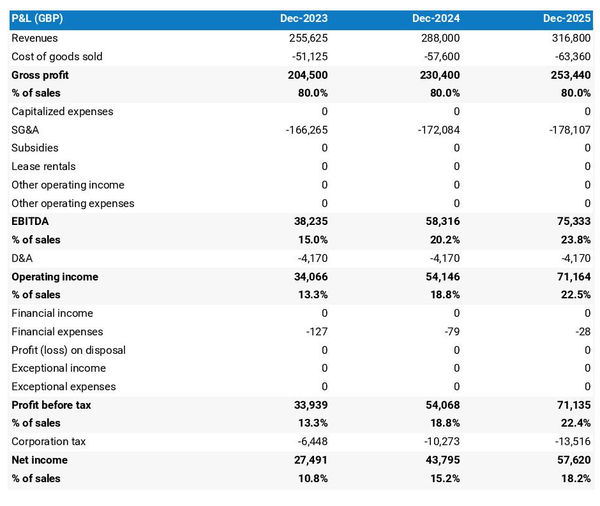

The projected P&L statement

The projected P&L statement for a mortgage broker shows how much revenue and profits your business is expected to generate in the future.

Ideally, your mortgage broker's P&L statement should show:

- Healthy growth - above inflation level

- Improving or stable profit margins

- Positive net profit

Expectations will vary based on the stage of your business. A startup will be expected to grow faster than an established mortgage broker. And similarly, an established company should showcase a higher level of profitability than a new venture.

The projected balance sheet of your mortgage broker

Your mortgage broker's forecasted balance sheet enables the reader of your plan to assess your financial structure, working capital, and investment policy.

It is composed of three types of elements: assets, liabilities and equity:

- Assets: represent what the business owns and uses to produce cash flows. It includes resources such as cash, equipment, and accounts receivable (money owed by clients).

- Liabilities: represent funds advanced to the business by lenders and other creditors. It includes items such as accounts payable (money owed to suppliers), taxes due and loans.

- Equity: is the combination of what has been invested by the business owners and the cumulative profits and losses generated by the business to date (which are called retained earnings). Equity is a proxy for the value of the owner's stake in the business.

Your mortgage broker's balance sheet will usually be analyzed in conjunction with the other financial statements included in your forecast.

Two key points of focus will be:

- Your mortgage broker's liquidity: does your business have sufficient cash and short-term assets to pay what it owes over the next 12 months?

- And its solvency: does your business have the capacity to repay its debt over the medium-term?

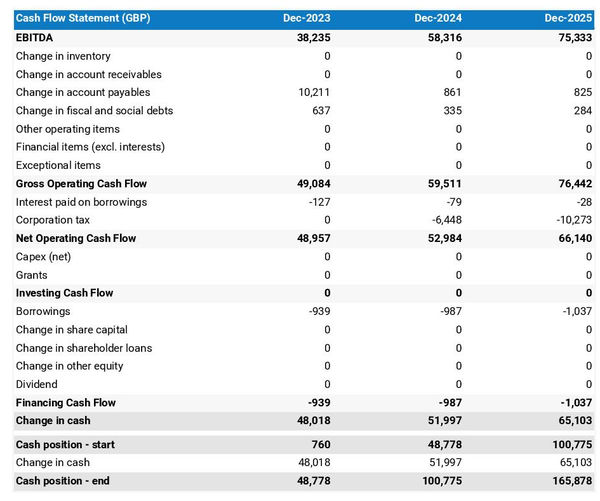

The projected cash flow statement

A cash flow forecast for a mortgage broker shows how much cash the business is projected to generate or consume.

The cash flow statement is divided into 3 main areas:

- The operating cash flow shows how much cash is generated or consumed by the operations (running the business)

- The investing cash flow shows how much cash is being invested in capital expenditure (equipment, real estate, etc.)

- The financing cash flow shows how much cash is raised or distributed to investors and lenders

Looking at the cash flow forecast helps you to ensure that your business has enough cash to keep running, and can help you anticipate potential cash shortfalls.

It is also a best practice to include a monthly cash flow statement in the appendices of your mortgage broker business plan so that the readers can view the impact of seasonality on your business cash position and generation.

The initial financing plan

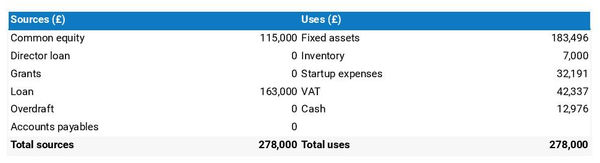

The initial financing plan, also known as a sources and uses table, is a valuable resource to have in your business plan when starting your mortgage broker as it reveals the origins of the money needed to establish the business (sources) and how it will be allocated (uses).

Having this table helps show what costs are involved in setting up your mortgage broker, how risks are shared between founders, investors and lenders, and what the starting cash position will be. This cash position needs to be sufficient to sustain operations until the business reaches a break-even point.

Now that you have a clear understanding of what goes into the financial forecast of your mortgage broker business plan, let's shift our focus to the written part of the plan.

Need a convincing business plan?

The Business Plan Shop makes it easy to create a financial forecast to assess the potential profitability of your projects, and write a business plan that’ll wow investors.

The written part of a mortgage broker business plan

The written part of the business plan is where you will explain what your business does and how it operates, what your target market is, whom you compete against, and what strategy you will put in place to seize the commercial opportunity you've identified.

Having this context is key for the reader to form a view on whether or not they believe that your plan is achievable and the numbers in your forecast realistic.

The written part of a mortgage broker business plan is composed of 7 main sections:

- The executive summary

- The presentation of the company

- The products and services

- The market analysis

- The strategy

- The operations

- The financial plan

Let's go through the content of each section in more detail!

1. The executive summary

The executive summary, the first section of your mortgage broker's business plan, serves as an inviting snapshot of your entire plan, leaving readers eager to know more about your business.

To compose an effective executive summary, start with a concise introduction of your business, covering its name, concept, location, history, and unique aspects. Share insights about the services or products you intend to offer and your target customer base.

Subsequently, provide an overview of your mortgage broker's addressable market, highlighting current trends and potential growth opportunities.

Then, present a summary of critical financial figures, such as projected revenues, profits, and cash flows.

You should then include a summary of your key financial figures such as projected revenues, profits, and cash flows.

Lastly, address any funding needs in the "ask" section of your executive summary.

2. The presentation of the company

As you build your mortgage broker business plan, the second section deserves attention as it delves into the structure and ownership, location, and management team of your company.

In the structure and ownership part, you'll provide valuable insights into the legal structure of the business, the identities of the owners, and their respective investments and ownership stakes. This level of transparency is vital, particularly if you're seeking financing, as it clarifies which legal entity will receive the funds and who holds the reins of the business.

Moving to the location part, you'll offer a comprehensive view of the company's premises and articulate why this specific location is strategic for the business, emphasizing factors like catchment area, accessibility, and nearby amenities.

When describing the location of your mortgage broker, you could indicate that it is located in a desirable area with access to many amenities and transportation options. It may be close to a major city, offering potential customers the convenience of being close to the city without having to live in a large, more expensive metropolitan area.

It could also be in an area with a low cost of living, making it more attractive to potential customers who are looking to save money. Moreover, it might be located near other businesses and shopping centers, allowing customers to have a variety of options for their needs.

Lastly, you should introduce your esteemed management team. Provide a thorough explanation of each member's role, background, and extensive experience.

It's equally important to highlight any past successes the management team has achieved and underscore the duration they've been working together. This information will instil trust in potential lenders or investors, showcasing the strength and expertise of your leadership team and their ability to deliver the business plan.

3. The products and services section

The products and services section of your mortgage broker business plan should include a detailed description of what your company sells to its customers.

For example, your mortgage broker might offer services such as helping customers find the best mortgage option for their needs, providing advice on interest rates, repayment options, and other loan features, and helping customers secure the best loan rate. These services are designed to help customers make informed decisions and secure the best deal possible.

The reader will want to understand what makes your mortgage broker unique from other businesses in this competitive market.

When drafting this section, you should be precise about the categories of products or services you sell, the clients you are targeting and the channels that you are targeting them through.

4. The market analysis

When you present your market analysis in your mortgage broker business plan, it's crucial to include detailed information about customers' demographics and segmentation, target market, competition, barriers to entry, and any relevant regulations.

The main objective of this section is to help the reader understand the size and attractiveness of the market while demonstrating your solid understanding of the industry.

Begin with the demographics and segmentation subsection, providing an overview of the addressable market for your mortgage broker, the key trends in the marketplace, and introducing different customer segments along with their preferences in terms of purchasing habits and budgets.

Next, focus on your target market, zooming in on the specific customer segments your mortgage broker aims to serve and explaining how your products and services fulfil their distinct needs.

For example, your target market might include first-time home buyers. This segment tends to be younger individuals who are looking to purchase their first home and need guidance on the best mortgage options, financial advice, and education on the home-buying process.

First-time home buyers often have a variety of questions, so having a mortgage broker who can provide them with the information and resources they need can be invaluable.

Then proceed to the competition subsection, where you introduce your main competitors and highlight what sets you apart from them.

Finally, conclude your market analysis with an overview of the key regulations applicable to your mortgage broker.

5. The strategy section

When writing the strategy section of a business plan for your mortgage broker, it is essential to include information about your competitive edge, pricing strategy, sales & marketing plan, milestones, and risks and mitigants.

The competitive edge subsection should explain what sets your company apart from its competitors. This part is especially key if you are writing the business plan of a startup, as you have to make a name for yourself in the marketplace against established players.

The pricing strategy subsection should demonstrate how you intend to remain profitable while still offering competitive prices to your customers.

The sales & marketing plan should outline how you intend to reach out and acquire new customers, as well as retain existing ones with loyalty programs or special offers.

The milestones subsection should outline what your company has achieved to date, and its main objectives for the years to come - along with dates so that everyone involved has clear expectations of when progress can be expected.

The risks and mitigants subsection should list the main risks that jeopardize the execution of your plan and explain what measures you have taken to minimize these. This is essential in order for investors or lenders to feel secure in investing in your venture.

Your mortgage broker may face the risk of losing clients due to market changes. For example, if the interest rates suddenly increase, some clients may find it difficult to afford the new rate and may choose to go with another broker.

Your mortgage broker may also face the risk of financial losses due to errors in calculations. For example, if the broker makes a mistake in the calculations for the loan, they could end up losing money in the process.

6. The operations section

In your business plan, it's also essential to provide a detailed overview of the operations of your mortgage broker.

Start by covering your team, highlighting key roles and your recruitment plan to support the expected growth. Outline the qualifications and experience required for each role and your intended recruitment methods, whether through job boards, referrals, or headhunters.

Next, clearly state your mortgage broker's operating hours, allowing the reader to assess staffing levels adequately. Additionally, mention any plans for varying opening times during peak seasons and how you'll handle customer queries outside normal operating hours.

Then, shift your focus to the key assets and intellectual property (IP) necessary for your business. If you rely on licenses, trademarks, physical structures like equipment or property, or lease agreements, make sure to include them in this section.

You may have key assets such as customer contact information and market data that could be valuable intellectual property. Additionally, you might also have proprietary software or unique processes that could provide a competitive advantage in the mortgage market.

Lastly, include a list of suppliers you plan to work with, detailing their services and main commercial terms, such as price, payment terms, and contract duration. Investors are interested in understanding why you've chosen specific suppliers, which may be due to higher-quality products or established relationships from previous ventures.

7. The presentation of the financial plan

The financial plan section is where we will include the financial forecast we talked about earlier in this guide.

Now that you have a clear idea of the content of a mortgage broker business plan, let's look at some of the tools you can use to create yours.

What tool should I use to write my mortgage broker's business plan?

In this section, we will be reviewing the two main solutions for creating a mortgage broker business plan:

- Using specialized online business plan software,

- Outsourcing the plan to the business plan writer.

Using an online business plan software for your mortgage broker's business plan

Using online business planning software is the most efficient and modern way to create a mortgage broker business plan.

There are several advantages to using specialized software:

- You can easily create your financial forecast by letting the software take care of the financial calculations for you without errors

- You are guided through the writing process by detailed instructions and examples for each part of the plan

- You can access a library of dozens of complete business plan samples and templates for inspiration

- You get a professional business plan, formatted and ready to be sent to your bank or investors

- You can easily track your actual financial performance against your financial forecast

- You can create scenarios to stress test your forecast's main assumptions

- You can easily update your forecast as time goes by to maintain visibility on future cash flows

- You have a friendly support team on standby to assist you when you are stuck

If you're interested in using this type of solution, you can try The Business Plan Shop for free by signing up here.

Need a convincing business plan?

The Business Plan Shop makes it easy to create a financial forecast to assess the potential profitability of your projects, and write a business plan that’ll wow investors.

Hiring a business plan writer to write your mortgage broker's business plan

Outsourcing your mortgage broker business plan to a business plan writer can also be a viable option.

Business plan writers are skilled in creating error-free business plans and accurate financial forecasts. Moreover, hiring a consultant can save you valuable time, allowing you to focus on day-to-day business operations.

However, it's essential to be aware that hiring business plan writers will be expensive, as you're not only paying for their time but also the software they use and their profit margin.

Based on experience, you should budget at least £1.5k ($2.0k) excluding tax for a comprehensive business plan, and more if you require changes after initial discussions with lenders or investors.

Also, exercise caution when seeking investment. Investors prefer their funds to be directed towards business growth rather than spent on consulting fees. Therefore, the amount you spend on business plan writing services and other consulting services should be insignificant compared to the amount raised.

Keep in mind that one drawback is that you usually don't own the business plan itself; you only receive the output, while the actual document is saved in the consultant's business planning software. This can make it challenging to update the document without retaining the consultant's services.

For these reasons, carefully consider outsourcing your mortgage broker business plan to a business plan writer, weighing the advantages and disadvantages of seeking outside assistance.

Why not create your mortgage broker's business plan using Word or Excel?

I must advise against using Microsoft Excel and Word (or their Google, Apple, or open-source equivalents) to write your mortgage broker business plan. Let me explain why.

Firstly, creating an accurate and error-free financial forecast on Excel (or any spreadsheet) is highly technical and requires a strong grasp of accounting principles and financial modelling skills. It is, therefore, unlikely that anyone will fully trust your numbers unless you have both a degree in finance and accounting and significant financial modelling experience, like us at The Business Plan Shop.

Secondly, relying on spreadsheets is inefficient. While it may have been the only option in the past, technology has advanced significantly, and software can now perform these tasks much faster and with greater accuracy. With the rise of AI, software can even help us detect mistakes in forecasts and analyze the numbers for better decision-making.

And with the rise of AI, software is also becoming smarter at helping us detect mistakes in our forecasts and helping us analyse the numbers to make better decisions.

Moreover, software makes it easier to compare actuals versus forecasts and maintain up-to-date forecasts to keep visibility on future cash flows, as we discussed earlier in this guide. This task is cumbersome when using spreadsheets.

Now, let's talk about the written part of your mortgage broker business plan. While it may be less error-prone, using software can bring tremendous gains in productivity. Word processors, for example, lack instructions and examples for each part of your business plan. They also won't automatically update your numbers when changes occur in your forecast, and they don't handle formatting for you.

Overall, while Word or Excel may seem viable for some entrepreneurs to create a business plan, it's by far becoming an antiquated way of doing things.

Takeaways

- Using business plan software is a modern and cost-effective way of writing and maintaining business plans.

- A business plan is not a one-shot exercise as maintaining it current is the only way to keep visibility on your future cash flows.

- A business plan has 2 main parts: a financial forecast outlining the funding requirements of your mortgage broker and the expected growth, profits and cash flows for the next 3 to 5 years; and a written part which gives the reader the information needed to decide if they believe the forecast is achievable.

We hope that this in-depth guide met your expectations and that you now have a clear understanding of how to write your mortgage broker business plan. Do not hesitate to contact our friendly team if you have questions additional questions we haven't addressed here.

Also on The Business Plan Shop

- How to write a business plan to secure a bank loan?

- Business planning advice

- Do i need a business plan?

- Business model and business plan: the difference explained

- Key steps to write a business plan?

- Top mistakes to avoid in your business plan

Do you know entrepreneurs interested in starting or growing a mortgage broker? Share this article with them!

Founder & CEO at The Business Plan Shop Ltd