How to create a financial forecast for a buy-to-let business?

If you are serious about keeping visibility on your future cash flows, then you need to build and maintain a financial forecast for your buy-to-let business.

Putting together a buy-to-let business financial forecast may sound complex, but don’t worry, with the right tool, it’s easier than it looks, and The Business Plan Shop is here to guide you.

In this practical guide, we'll cover everything you need to know about building financial projections for your buy-to-let business.

We will start by looking at why they are key, what information is needed, what a forecast looks like once completed, and what solutions you can use to create yours.

Let's dive in!

Why create and maintain a financial forecast for a buy-to-let business?

In order to prosper, your business needs to have visibility on what lies ahead and the right financial resources to grow. This is where having a financial forecast for your buy-to-let business becomes handy.

Creating a buy-to-let business financial forecast forces you to take stock of where your business stands and where you want it to go.

Once you have clarity on the destination, you will need to draw up a plan to get there and assess what it means in terms of future profitability and cash flows for your buy-to-let business.

Having this clear plan in place will give you the confidence needed to move forward with your business’s development.

Having an up-to-date financial forecast for a buy-to-let business is also useful if your trading environment worsens, as the forecast enables you to adjust to your new market conditions and anticipate any potential cash shortfall.

Finally, your buy-to-let business's financial projections will also help you secure financing, as banks and investors alike will want to see accurate projections before agreeing to finance your business.

Need a convincing business plan?

The Business Plan Shop makes it easy to create a financial forecast to assess the potential profitability of your projects, and write a business plan that’ll wow investors.

What information is used as input to build a buy-to-let business financial forecast?

A buy-to-let business's financial forecast needs to be built on the right foundation: your assumptions.

The data required to create your assumptions will depend on whether you are a new or existing buy-to-let business.

If you are creating (or updating) the forecast of an existing buy-to-let business, then your main inputs will be historical accounting data and operating metrics, and your team’s view on what to expect for the next three to five years.

If you are building financial projections for a new buy-to-let business startup, you will need to rely on market research to form your go-to-market strategy and derive your sales forecast.

For a new venture, you will also need an itemised list of resources needed for the buy-to-let business to operate, along with a list of equipment required to launch the venture (more on that below).

Now that you understand what is needed, let’s have a look at what elements will make up your buy-to-let business's financial forecast.

The sales forecast for a buy-to-let business

From experience, it is usually best to start creating your buy-to-let business financial forecast by your sales forecast.

To create an accurate sales forecast for your buy-to-let business, you will have to rely on the data collected in your market research, or if you're running an existing buy-to-let business, the historical data of the business, to estimate two key variables:

- The average price

- The number of monthly transactions

To get there, you will need to consider the following factors:

- Changes in interest rates set by the central bank can have a significant impact on the average price of your buy-to-let properties. When interest rates are low, it becomes more affordable for potential buyers to take out loans, increasing demand and driving up prices. On the other hand, when interest rates are high, it may deter buyers from making purchases, resulting in lower prices.

- The state of the economy can also affect the average price of your properties. During an economic recession, people may be less likely to invest in property, leading to a decrease in prices. Conversely, during times of economic growth, more people may have the means to invest in property, driving up prices.

- Government policies related to the housing market can also influence the average price of your properties. For example, changes in tax laws or regulations on rental properties can impact the overall demand and pricing for buy-to-let properties.

- The supply of properties in the market can affect the average price of your properties. If there is a high demand for rental properties and a limited supply, you may be able to charge higher prices for your properties. However, if there is an oversupply of rental properties, it can lead to lower prices as tenants have more options to choose from.

- The location of your properties can have a significant impact on the average price and number of monthly transactions. Properties in desirable locations, such as near schools, public transportation, and amenities, may command higher prices and attract more potential tenants, resulting in a higher number of transactions.

Once you have an idea of what your future sales will look like, it will be time to work on your overhead budget. Let’s see what this entails.

Need a convincing business plan?

The Business Plan Shop makes it easy to create a financial forecast to assess the potential profitability of your projects, and write a business plan that’ll wow investors.

The operating expenses for a buy-to-let business

The next step is to estimate the costs you’ll have to incur to operate your buy-to-let business.

These will vary based on where your business is located, and its overall size (level of sales, personnel, etc.).

But your buy-to-let business's operating expenses should normally include the following items:

- Mortgage payments: As a buy-to-let business owner, one of your main operating expenses will be your monthly mortgage payments. This is the cost of financing your rental property and can vary depending on your interest rate and loan terms.

- Property taxes: You are responsible for paying property taxes on your rental property. These taxes can vary depending on the location and value of your property.

- Maintenance and repairs: As a landlord, you are responsible for maintaining your rental property. This includes regular upkeep such as painting, landscaping, and fixing any issues that may arise.

- Utilities: Depending on your rental agreement, you may be responsible for paying certain utilities such as water, electricity, and gas for your tenants.

- Insurance: It is important to have insurance coverage for your rental property to protect yourself from any potential damages or liabilities.

- Accountancy fees: As a business owner, you will need to hire an accountant to help you with your taxes and financial statements. This can be a recurring expense throughout the year.

- Property management fees: If you choose to hire a property management company to handle day-to-day operations, you will incur fees for their services.

- Advertising and marketing: To attract tenants, you may need to invest in advertising and marketing efforts such as listing your property on rental websites or hiring a real estate agent.

- Software licenses: As a buy-to-let business owner, you may need to invest in software licenses for property management, accounting, or other business purposes.

- Banking fees: You will likely have a business bank account for your rental property, and there may be fees associated with maintaining this account.

- Legal fees: It is important to have legal counsel for your buy-to-let business, especially when dealing with contracts and potential disputes with tenants.

- Cleaning services: If you do not have the time or resources to clean your rental property yourself, you may need to hire a professional cleaning service to maintain the cleanliness of the property.

- HOA fees: If your rental property is part of a homeowners association, you will be responsible for paying any associated fees.

- Licenses and permits: Depending on your location, you may need to obtain certain licenses and permits to operate your buy-to-let business.

- Legal compliance costs: As a landlord, you are responsible for complying with all relevant laws and regulations, which may result in additional costs such as inspections or certifications.

This list is not exhaustive by any means, and will need to be tailored to your buy-to-let business's specific circumstances.

What investments are needed to start or grow a buy-to-let business?

Your buy-to-let business financial forecast will also need to include the capital expenditures (aka investments in plain English) and initial working capital items required for the creation or development of your business.

For a buy-to-let business, these could include:

- Property Purchase: This is the initial cost of purchasing the property that you plan to rent out. It includes the down payment, closing costs, and any other fees associated with the purchase.

- Renovations and Repairs: As a landlord, it is your responsibility to maintain the property and keep it in good condition for your tenants. This may include major renovations such as updating the kitchen or bathroom, or smaller repairs like fixing a leaky faucet.

- Furnishings and Appliances: If you plan to rent out your property as a furnished rental, you will need to purchase furniture and appliances for your tenants to use. This can include items such as beds, sofas, refrigerators, and stoves.

- Property Management Fees: If you choose to hire a property management company to handle the day-to-day operations of your rental property, their fees should be included in your expenditure forecast. This can include fees for finding and screening tenants, collecting rent, and managing repairs and maintenance.

- Landlord Insurance: As a landlord, it is important to protect your investment with landlord insurance. This type of insurance provides coverage for any damage to your property, liability protection, and loss of rental income in case of a disaster or tenant default.

Again, this list will need to be adjusted according to the size and ambitions of your buy-to-let business.

Need a convincing business plan?

The Business Plan Shop makes it easy to create a financial forecast to assess the potential profitability of your projects, and write a business plan that’ll wow investors.

The financing plan of your buy-to-let business

The next step in the creation of your financial forecast for your buy-to-let business is to think about how you might finance your business.

You will have to assess how much capital will come from shareholders (equity) and how much can be secured through banks.

Bank loans will have to be modelled so that you can separate the interest expenses from the repayments of principal, and include all this data in your forecast.

Issuing share capital and obtaining a bank loan are two of the most common ways that entrepreneurs finance their businesses.

What tables compose the financial plan for a buy-to-let business?

Now let's have a look at the main output tables of your buy-to-let business's financial forecast.

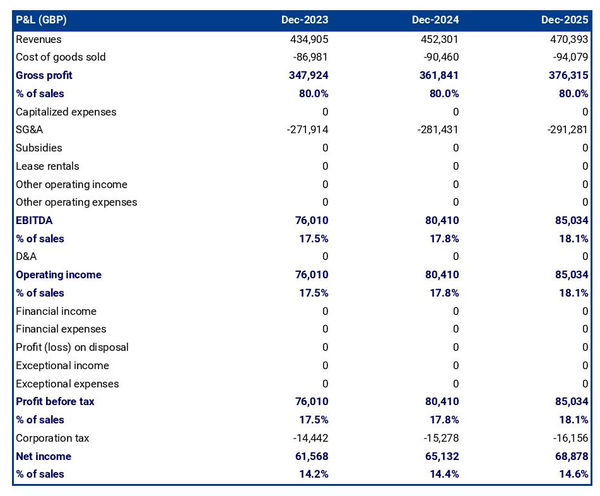

The forecasted profit & loss statement

The profit & loss forecast gives you a clear picture of your business’ expected growth over the first three to five years, and whether it’s likely to be profitable or not.

A healthy buy-to-let business's P&L statement should show:

- Sales growing at (minimum) or above (better) inflation

- Stable (minimum) or expanding (better) profit margins

- A healthy level of net profitability

This will of course depend on the stage of your business: numbers for an established buy-to-let business will look different than for a startup.

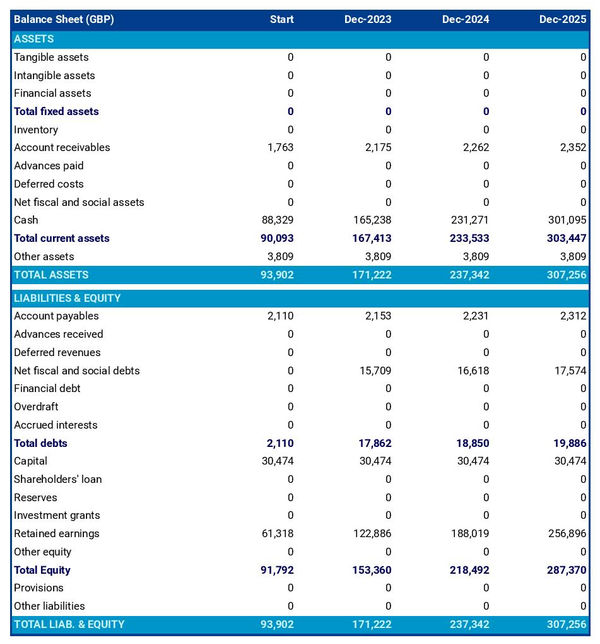

The projected balance sheet

The projected balance sheet gives an overview of your buy-to-let business's financial structure at the end of the financial year.

It is composed of three categories of items: assets, liabilities and equity:

- Assets: are what the business possesses and uses to produce cash flows. It includes resources such as cash, buildings, equipment, and accounts receivable (money owed by clients).

- Liabilities: are the debts of your buy-to-let business. They include accounts payable (money owed to suppliers), taxes due and bank loans.

- Equity: is the combination of what has been invested by the business owners and the cumulative profits to date (which are called retained earnings). Equity is a proxy for the value of the owner's stake in the business.

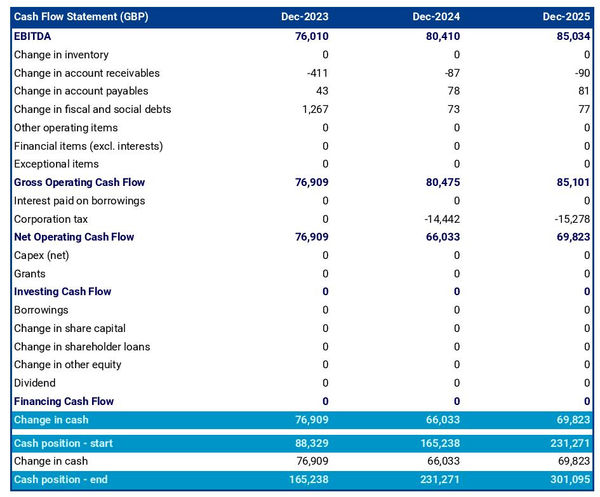

The projected cash flow statement

A projected cash flow statement for a buy-to-let business is used to show how much cash the business is generating or consuming.

The cash flow forecast is usually organised by nature to show three key metrics:

- The operating cash flow: do the core business activities generate or consume cash?

- The investing cash flow: how much is the business investing in long-term assets (this is usually compared to the level of fixed assets on the balance sheet to assess whether the business is regularly maintaining and renewing its equipment)?

- The financing cash flow: is the business raising new financing or repaying financiers (debt repayment, dividends)?

Cash is king and keeping an eye on future cash flows is imperative for running a successful business. Therefore, you should pay close attention to your buy-to-let business's cash flow forecast.

If you are trying to secure financing, note that it is customary to provide both yearly and monthly cash flow forecasts in a financial plan - so that the reader can analyze seasonal variation and ensure the buy-to-let business is appropriately capitalised.

Need a convincing business plan?

The Business Plan Shop makes it easy to create a financial forecast to assess the potential profitability of your projects, and write a business plan that’ll wow investors.

Which tool should you use to create your buy-to-let business's financial forecast?

Creating your buy-to-let business's financial forecast may sound fairly daunting, but the good news is that there are several ways to go about it.

Using online financial forecasting software to build your buy-to-let business's projections

The modern and easiest way is to use an online financial forecasting tool such as the one we offer at The Business Plan Shop.

There are several advantages to using specialised software:

- You can easily create your financial forecast by letting the software take care of the financial calculations for you without errors

- You have access to complete financial forecast templates

- You get a complete financial forecast ready to be sent to your bank or investors

- You can easily track your actual financial performance against your financial forecast, and recalibrate your forecast as the year goes by

- You can create scenarios to stress test your forecast's main assumptions

- You can easily update your forecast as time goes by to maintain visibility on future cash flows

- You have a friendly support team on standby to assist you when you are stuck

- It’s cost-efficient and much cheaper than using an accountant or consultant (see below)

If you are interested in this type of solution, you can try our projection software for free by signing up here.

Hiring a financial consultant or chartered accountant

Hiring a consultant or chartered accountant is also an efficient way to get a professional buy-to-let business financial projection.

As you can imagine, this solution is much more expensive than using software. From experience, the creation of a simple financial forecast over three years (including a balance sheet, income statement, and cash flow statement) is likely to start around £700 or $1,000 excluding taxes.

The indicative estimate above, is for a small business, and a forecast done as a one-off. Using a financial consultant or accountant to track your actuals vs. forecast and to keep your financial forecast up to date on a monthly or quarterly basis will naturally cost a lot more.

If you choose this solution, make sure your service provider has first-hand experience in your industry, so that they may challenge your assumptions and offer insights (as opposed to just taking your figures at face value to create the forecast’s financial statements).

Why not use a spreadsheet such as Excel or Google Sheets to build your buy-to-let business's financial forecast?

You and your financial partners need numbers you can trust. Unless you have studied finance or accounting, creating a trustworthy and error-free buy-to-let business financial forecast on a spreadsheet is likely to prove challenging.

Financial modelling is very technical by nature and requires a solid grasp of accounting principles to be done without errors. This means that using spreadsheet software like Excel or Google Sheets to create accurate financial forecasts is out of reach for most business owners.

Creating forecasts in Excel is also inefficient nowadays:

- Software has advanced to the point where forecasting can be done much faster and more accurately than manually on a spreadsheet.

- With artificial intelligence, the software is capable of detecting mistakes and helping decision-making.

Spreadsheets are versatile tools but they are not tailor-made for reporting. Importing your buy-to-let business's accounting data in Excel to track actual vs. forecast is incredibly manual and tedious (and so is keeping forecasts up to date). It is much faster to use dedicated financial planning tools like The Business Plan Shop which are built specially for this.

Need a convincing business plan?

The Business Plan Shop makes it easy to create a financial forecast to assess the potential profitability of your projects, and write a business plan that’ll wow investors.

Use our financial projection templates for inspiration

The Business Plan Shop has dozens of financial forecast templates available.

Our examples contain a complete business plan with a financial forecast and a written presentation of the company, the team, the strategy, and the medium-term objectives.

Whether you are just starting out or already have your own buy-to-let business, looking at our financial forecast template is a good way to:

- Understand what a complete business plan should look like

- Understand how you should model financial items for your buy-to-let business

Takeaways

- A financial projection shows expected growth, profitability, and cash generation for your business over the next three to five years.

- Tracking actuals vs. forecast and keeping your financial forecast up-to-date is the only way to maintain visibility on future cash flows.

- Using financial forecasting software makes it easy to create and maintain up-to-date projections for your buy-to-let business.

You have reached the end of our guide. We hope you now have a better understanding of how to create a financial forecast for a buy-to-let business. Don't hesitate to contact our team if you have any questions or want to share your experience building forecasts!

Need a convincing business plan?

The Business Plan Shop makes it easy to create a financial forecast to assess the potential profitability of your projects, and write a business plan that’ll wow investors.

Also on The Business Plan Shop

- Example of financial projections

- How to create a turnover forecast for a business?

- Financial forecast template for a business idea

Know someone who runs or wants to start a buy-to-let business? Share our financial projection guide with them!

Founder & CEO at The Business Plan Shop Ltd