How to open an insurance brokerage firm?

Are you keen to open an insurance brokerage firm but don't know where to begin? Then you're in luck because this guide will lead you through all the steps required to check if your business idea can be profitable and, if so, turn it into a reality.

Our guide is for prospective entrepreneurs who are thinking about starting an insurance brokerage firm no matter how far they are in their journey - whether you’re just thinking about it or in the middle of market research this guide will be useful to you.

Think of this as your blueprint: we cover everything you need to know about opening an insurance brokerage firm and what key decisions you’ll need to make along the way.

Ready? Let’s get started!

Learn how an insurance brokerage firm works

Before you can start an insurance brokerage firm, you need to have a solid understanding of how the business works and what are its main revenue streams.

This will give you a glimpse into the profitability potential of your venture, whilst allowing you to decide whether or not it is a good fit for your situation (current skill set, savings and capital available to start the business, and family responsibilities).

It may be that creating an insurance brokerage firm is an excellent idea, but just not the right one for you.

Before starting their own company, successful entrepreneurs typically:

- Consult with and take advice from experienced insurance brokerage firm owners

- Acquire hands-on experience by working in an operational insurance brokerage firm

- Take relevant training courses

Let's explore each option in a bit more detail.

Consulting with and taking advice from experienced insurance brokerage firm owners

Having "seen it all", established business owners can offer valuable insights and hands-on advice drawn from their own experiences.

This is because, through both successes and failures, they've gained a more informed and practical understanding of what it takes to build and sustain a successful insurance brokerage firm over the long term.

Acquiring hands-on experience by working in an operational insurance brokerage firm

If you want to open an insurance brokerage firm, having industry-specific experience is imperative because it equips you with the knowledge, network, and acumen necessary to navigate challenges and make informed decisions critical to the success of your future business.

You'll also be able to judge whether or not this business idea is suitable for you or if there might be conflicts of interest with your personal life (for example, long working hours could be incompatible with raising young children).

This work experience will also help you to make contacts in the industry and familiarise yourself with customers and their expectations, which will prove invaluable when you set up your insurance brokerage firm.

Take relevant training courses

Taking a training course is another way of familiarising yourself with the business model of your future activity before you decide to make the jump.

You may choose to complete a training course to obtain a certificate or degree, or just take online courses to acquire practical skills.

Before going any further in setting up your venture

Before you go any further with your plans to open an insurance brokerage firm, make sure you have a clear vision of what it will take in terms of:

- What skills are needed to run the business successfully (do you have some or all of these skills?)

- What a standard working week looks like (does it suit your personal commitments?)

- What sales potential and long-term growth prospects the insurance brokerage firm has (compare this with your level of ambition)

- What options you'll have once you decide to retire (or move on and inevitably sell the company)

This analysis of the business model and the constraints of the business should help you to check that your idea of launching an insurance brokerage firm fits your entrepreneurial profile.

If there is a match, it will then be time to look at assembling the founding team of your business.

Can your business idea be profitable?

Just enter your data and let The Business Plan Shop crunch the numbers. We will tell if your business idea can generate profits and cash flows, and how much you need to get started.

Assemble your insurance brokerage firm's founding team

The next step to start your insurance brokerage firm is to think about the ideal founding team, or to go in alone (which is always an option).

Setting up a business with several partners is a way of reducing the (high) risk of launching an insurance brokerage firm since it allows the financial risk of the project to be shared between the co-founders.

This also allows the company to benefit from a greater diversity of profiles in the management team and to spread the burden of decision-making over several shoulders.

But, running a business with multiple co-founders brings its own challenges. Disagreements between co-founders are quite common, and these can pose risks to the business. That's why it's crucial to consider all aspects before starting your business.

To make an informed decision, we suggest asking yourself these questions:

- How many co-founders would increase the project's chances of success?

- Do you and your potential partners share the same aspirations for the project?

- What is your plan B in case of failure?

Let's examine each of these questions in detail.

How many co-founders would increase the project's chances of success?

The answer to this question will depend on a number of factors, including:

- Your savings compared with the amount of initial capital needed to launch the insurance brokerage firm

- The skills you have compared with those needed to make a success of such a project

- How you want key decisions to be taken in the business (an odd number of partners or a majority partner is generally recommended to avoid deadlock)

Put simply, your partners contribute money and/or skills, and increasing the number of partners is often a good idea when one of these resources is in short supply.

Do you and your potential partners share the same aspirations for the project?

One of the key questions when selecting your potential partners will be their expectations. Do you want to create a small or large business? What are your ambitions for the next 10 or 15 years?

It's better to agree from the outset on what you want to create to avoid disagreements, and to check that you stay on the same wavelength as the project progresses to avoid frustration.

What is your plan B in case of failure?

Of course, we wish you every success, but it's wise to have a plan B when setting up a business.

How you handle the possibility of things not working out can depend a lot on the kind of relationship you have with your co-founders (like being a close friend, spouse, former colleague, etc.) and each person's individual situation.

Take, for instance, launching a business with your spouse. It may seem like a great plan, but if the business doesn't succeed, you could find yourself losing the entire household income at once, and that could be quite a nerve-wracking situation.

Similarly, starting a business partnership with a friend has its challenges. If the business doesn't work out or if tough decisions need to be made, it could strain the friendship.

It's essential to carefully evaluate your options before starting up to ensure you're well-prepared for any potential outcomes.

Undertake market research for an insurance brokerage firm

The next step to start your insurance brokerage firm is to check that there is indeed an opportunity to be seized, using market research. Let's take a look at what this involves.

The objectives of market research

In a nutshell, doing market research enables you to verify that there is a business opportunity for your company to seize, and to size the opportunity precisely.

First of all, market research enables you to assess whether the market you're targeting is large enough to withstand the arrival of a new competitor: your insurance brokerage firm.

The market analysis will also help you define the product and service offering of your insurance brokerage firm, and transcribe it into a market positioning and concept that will strike a chord with your target customers.

Finally, your market research will provide you with the data you need to draw up your sales and marketing plan and estimate the revenue potential of your insurance brokerage firm.

Analyse key trends in the industry

Market research for an insurance brokerage firm must always begin with a thorough investigation of consumer habits and current industry trends.

Normally, insurance brokerage firm market research begins with a sectorial analysis which will provide you with a better understanding of how the industry is organized, who the major players are, and what are the current market trends.

Assess the demand

A demand analysis enables you to accurately assess the expectations of your insurance brokerage firm's future customers.

Your analysis will focus on the following questions:

- How many potential customers are present in the geographical areas served by your company?

- What are their expectations and purchasing behaviors?

- How much are they willing to spend?

- Are there different customer segments with distinct characteristics?

- How to communicate and where to promote your business to reach your target market?

The main goal of your demand analysis is to identify potential customer segments that your insurance brokerage firm could target and what products or services would meet these customers' expectations.

Supply side

Supply-side analysis looks at the products and services offered by your competitors on the market.

You should focus here on the following questions:

- Who will your competitors be?

- Are they any good?

- Where are they located?

- Who do they target?

- What range of products and services do they offer?

- Are they independent players or part of a chain?

- What prices do they charge?

- How do they sell their products and services?

- Do their concepts appeal to customers?

One of the aims of your supply-side analysis will be to gather the elements that will enable you to define a market positioning that will set you apart from what is already being done on the market, so as to avoid direct confrontation with competitors already established (more on that below).

Regulations

Market research is also an opportunity to look at the regulations and conditions required to do business.

You should ask yourself the following questions:

- Does it take a specific degree to open an insurance brokerage firm?

- Do you need specific licences or business permits?

- What are the main regulations applicable to your future business?

Given that your project is still in its early stages, your analysis of the regulation can be carried out at a high level for the time being. You just want to identify the main laws applicable and check that you meet the conditions for running this type of business before going any further.

Once your project is more advanced, you can come back to the regulation in greater detail with your lawyer.

Concluding your market research

Your market research should lead you to draw a clear conclusion about your chances of commercial success of your business idea:

- Either the market is saturated, and you'd better look into another business idea.

- Or there's an opportunity to be seized in the geographical area you're considering, and you can go ahead with your project to open an insurance brokerage firm.

Need a convincing business plan?

The Business Plan Shop makes it easy to create a financial forecast and write a business plan to help convince investors that your business idea can be profitable.

Choose the right concept and position your insurance brokerage firm on the market

The next step to start an insurance brokerage firm is to choose the company's market positioning.

Market positioning refers to the place your product and service offering occupies in customers' minds and how it differs from how competitors are perceived. Being perceived as a high-end solution, for example.

To do this, you need to take the following considerations into account:

- How can you make your business stand out from your competitors?

- Can you consider joining a franchise as a way to lower the risks involved?

- Is it better to start a new insurance brokerage firm or acquire one that is already up and running?

- How to make sure your concept meets customer needs?

Let's look at each of these in a little more detail.

How can you make your business stand out from your competitors?

When you decide to start your own insurance brokerage firm, you're facing an upward challenge because your competitors are already ahead. They have a good reputation, loyal customers, and a strong team, while you're just getting started.

Opening an insurance brokerage firm offering exactly the same thing as your competitors is risky and potentially doomed to fail: why would customers take the risk of choosing a newcomer rather than a company with a proven track record?

This is why it is advisable to avoid direct confrontation by adopting a differentiated market positioning wherever possible: in other words, by offering something different or complementary to what is available on the market.

To find a market positioning that has every chance of success, you need to ask yourself the following questions:

- Can you negate direct competition by serving a customer profile that is currently poorly addressed by your competitors?

- Can your business provide something different or complementary to what is already available on the market?

- Why will customers choose your insurance brokerage firm over the competition?

- How will your competitors react to your entry into their market?

- Is the market sufficiently large and fragmented (i.e. not dominated by a few large chains) to allow you to set up an independent business, or is it better to consider another avenue (see below)?

Can you consider joining a franchise as a way to lower the risks involved?

A good way of getting a market positioning that is guaranteed to seduce customers is to join a group with a proven concept.

Admittedly, joining a franchise is not necessarily as exciting as opening an insurance brokerage firm with a clean slate, everything to invent and total freedom to do so, but it is a proven way of reducing the risk of entering the market.

By joining a franchise, you will benefit from a concept that is successful with customers, the brand recognition of a large network, and operational support with regard to supplier relations, processes and operating standards, etc.

In return, you will have to pay an entry fee and an annual royalty (on your company's sales).

Joining a franchise is a trade-off where you need additional capital and get less freedom in exchange for a lot less risk. It's not for everyone, and it's not possible everywhere (franchise opportunities vary from region to region), but it is nevertheless an option you should explore.

Is it better to start a new insurance brokerage firm or acquire one that is already up and running?

Another way to benefit from a proven concept and reduce the risk of your project is to take over an insurance brokerage firm.

Buying an insurance brokerage firm allows you to get a team, a customer base, and above all to preserve the balance on the market by avoiding creating a new player. For these reasons, taking over a business is a lot less risky than creating one from scratch.

Taking over a business also gives you greater freedom than franchising, because you have the freedom to change the positioning and operations of the business as you see fit.

However, as you can imagine, the cost of taking over a business is higher than that of opening an insurance brokerage firm because you will have to finance the purchase.

How to make sure your concept meets customer needs?

Once you have decided on your concept and the market positioning of your future insurance brokerage firm, you will need to check that it meets the needs, expectations and desires of your future customers.

To do this, you need to present it to some of your target customers to gather their impressions.

Explore the ideal location to start your insurance brokerage firm

The next stage in our guide on how to start an insurance brokerage firm: choosing where to set up shop.

Setting up your business in the right location will have a direct impact on your chances of success, so it's a good idea to think things through before you launch.

To help you decide where to set up your business, we recommend considering the following factors:

- Visibility and foot traffic - Insurance brokerage firms rely on building relationships and attracting potential clients, so it is important for them to be located in a visible and high foot traffic area.

- Parking space, road and public transport accessibility - Clients may drive to the firm's office for meetings, so having ample parking space and easy access to main roads is important. Public transport accessibility can also make it easier for employees to commute to work.

- Proximity to target customers - Insurance brokerage firms often target a specific demographic or industry, so it is important for them to be located near their target customers.

- Competitor presence - While having competitors nearby may seem like a disadvantage, it can also indicate that the area is in high demand for insurance services, making it a potentially profitable location for the firm.

These criteria will need to be refined according to the specific features of your project.

After weighing the factors mentioned earlier, it's crucial to focus on your startup's budget. Look for a location that suits your business needs while being affordable, especially in the short term.

One of the issues that will also come up is the long-term future of your location, particularly if you opt to rent your premises rather than buy. In this case, you will need to consider the conditions for renewing the lease (duration, rent increases, etc.).

Lease agreements vary widely from country to country, so make sure you check the terms applicable to your situation and have your lawyer review your lease before you sign.

Need inspiration for your business plan?

Avoid writer's block and draft your own business plan in no time by drawing inspiration from dozens of business plan templates.

Decide on a legal form for your insurance brokerage firm

It's now time to think about the legal structure for your insurance brokerage firm.

The legal form of a business simply means the legal structure it operates under. This structure outlines how the business is set up and defines its legal obligations and responsibilities.

What are the most common legal structures?

Naturally, the names and intricacies of business structures differ by country. However, they typically fit into two main categories:

- Individual businesses

- Companies

Individual businesses

Individual businesses are usually a good fit for self-employed individuals and freelancers who want limited administrative work. These types of entrepreneurs are commonly referred to as sole traders or sole proprietorships.

As mentioned above, the main benefit of being a sole trader is that minimal paperwork is required to launch and operate the business. Tax calculations are also relatively simple and annual accounts are not always required (and when they are, usually don't need to be audited) which saves a bit of time and money on bookkeeping and accounting fees.

Decision-making is also easy as the final decision is fully dependent on the sole trader (even if employees are hired).

However, being a sole trader also has drawbacks. The main disadvantage is that there is no separation between the individual running day-to-day operations and the business.

This means that if the business were to file for bankruptcy or legal disputes were to arise, the individual would be liable for any debts and their personal assets subsequently at risk. In essence, sole traders have unlimited liability.

This also means that profits earned by the business are usually taxed under the personal income tax category of the sole trader.

Another drawback is that sole traders might find it harder to finance their business. Debt (bank loan for example) is likely to be the only source of external financing given that the business doesn't have a share capital (effectively preventing equity investors from investing in their business).

Companies

Companies are more flexible and more robust than individual businesses. They are suitable for projects of all sizes and can be formed by one or more individuals, working on their own or with employees.

Unlike individual businesses, companies are recognised as distinct entities that have their own legal personality. Usually, there is also a limited liability which means that founders and investors cannot lose more than the capital they have invested into the business.

This means that there is a clear legal separation between the company and its owners (co-founders and investors), which protects the latter's personal assets in the event of legal disputes or bankruptcy.

Entrepreneurs using companies also gain the advantage of being able to attract equity investment by selling shares in the business.

As you can see companies offer better protection and more financing options, but this comes at a trade-off in terms of red-tape and complexity.

From a taxation perspective, companies are usually liable for corporation tax on their profits, and the income received by the owners running the business is taxed separately (like normal employees).

Normally, companies also have to produce annual accounts, which might have to be audited, and hold general assemblies, among other formalities.

How should I choose my insurance brokerage firm's legal setup?

Choosing the right legal setup is often simple once you figure out things like how many partners you'll have, if you hire employees, and how much money you expect to make.

Remember, a great business idea can work well no matter which legal structure you pick. Tax laws change often, so you shouldn't rely too much on getting specific tax benefits from a certain structure when getting started.

You could start by looking at the legal structures most commonly utilised by your competitors. As your idea evolves and you're ready to officially register your business, it's a good idea to confirm your choice using inputs from a lawyer and an accountant.

Can I switch my insurance brokerage firm's legal structure if I get it wrong?

Yes, you have the flexibility to change your legal setup later, which might include selling the existing one and adopting a new structure in certain situations. Keep in mind, though, that this restructuring comes with additional expenses, so making the right choice from the start is usually more cost-effective.

Can your business idea be profitable?

Just enter your data and let The Business Plan Shop crunch the numbers. We will tell if your business idea can generate profits and cash flows, and how much you need to get started.

Assess the startup costs for an insurance brokerage firm

The next step in creating an insurance brokerage firm involves thinking about the equipment and staff needed for the business to operate.

After figuring out what you need for your business, your financial plan will reveal how much money you'll need to start and how much you might make (check below for more details).

Because every venture is distinctive, providing a reliable one-size-fits-all budget for launching an insurance brokerage firm without knowing the specifics of your project is not feasible.

Each project has its own particularities (size, concept, location), and only a forecast can show the exact amount required for the initial investment.

The first thing you'll need to consider is the equipment and investments you'll need to get your business up and running.

Startup costs and investments to launch your insurance brokerage firm

For an insurance brokerage firm, the initial working capital requirements (WCR) and investments could include the following elements:

- Office Space: As an insurance brokerage firm, you will need a dedicated office space to conduct business and meet with clients. This may include expenses such as rent or mortgage payments, utilities, and office furniture.

- Technology and Equipment: To efficiently run your business, you will need to invest in technology and equipment such as computers, printers, fax machines, and software. This will not only help with day-to-day operations, but also demonstrate to clients that you are a modern and professional firm.

- Insurance Licenses and Fees: In order to legally operate as an insurance brokerage firm, you will need to obtain licenses and pay fees to regulatory bodies. These expenses may include licensing exams, annual fees, and registration fees.

- Marketing Materials: While marketing and advertising expenses are not included in the expenditure forecast, you may need to invest in marketing materials such as business cards, brochures, and branded merchandise to promote your business and attract clients.

- Training and Development: While this may not fall under traditional capital expenditures, investing in the training and development of yourself and your employees is crucial for the success of your insurance brokerage firm. This may include attending conferences, workshops, or obtaining professional certifications.

Of course, you will need to adapt this list to your business specificities.

Staffing plan of an insurance brokerage firm

In addition to equipment, you'll also need to consider the human resources required to run the insurance brokerage firm on a day-to-day basis.

The number of recruitments you need to plan will depend mainly on the size of your company.

Once again, this list is only indicative and will need to be adjusted according to the specifics of your insurance brokerage firm.

Other operating expenses for an insurance brokerage firm

While you're thinking about the resources you'll need, it's also a good time to start listing the operating costs you'll need to anticipate for your business.

The main operating costs for an insurance brokerage firm may include:

- Staff Costs: This includes salaries, bonuses, benefits, and training expenses for your employees.

- Accountancy Fees: You will need to hire an accountant to help you manage your financial records and prepare tax returns.

- Insurance Costs: As an insurance brokerage firm, you will need to purchase professional liability insurance and other types of insurance to protect your business.

- Software Licenses: You will need to purchase software licenses for various programs and platforms to manage client information, process payments, and track sales.

- Banking Fees: You will incur fees for maintaining business bank accounts, processing transactions, and using other banking services.

- Rent: You will need to rent office space to operate your business.

- Marketing and Advertising Expenses: You will need to promote your services through various channels, such as social media, print ads, and events.

- Travel Expenses: You may need to travel to meet with clients, attend industry conferences, or conduct market research.

- Office Supplies: You will need to purchase office supplies, such as paper, ink, and stationery, to keep your business running smoothly.

- Professional Memberships: You may need to join professional organizations or associations to network and stay updated on industry trends.

- Technology Expenses: You will need to invest in technology, such as computers, printers, and servers, to support your operations.

- Legal Fees: You may need to consult with a lawyer for legal advice or to review contracts and agreements.

- Office Maintenance: You will need to cover expenses for office cleaning, repairs, and maintenance.

- Employee Benefits: In addition to salaries, you may offer benefits such as health insurance, retirement plans, and paid time off to attract and retain top talent.

- Utilities: You will need to pay for utilities, such as electricity, water, and internet, to keep your office running.

Like for the other examples included in this guide, this list will need to be tailored to your business but should be a good starting point for your budget.

Creating a sales & marketing plan for your insurance brokerage firm

The next step to start an insurance brokerage firm is to think about how you are going to attract and retain customers.

You need to ask yourself the following questions:

- What actions can be leveraged to attract as many customers as possible?

- How will you then retain customers?

- What resources do you need to allocate for each initiative (human and financial)?

- How many sales and what turnover can you expect to generate in return?

How you will attract and retain customers depends on your ambition, the size of your startup and the nature of your exact concept, but you could consider the following initiatives.

Your sales forecast may also be influenced by seasonality related to your business type, such as fluctuations during busy holiday periods, and your competitive environment.

Can your business idea be profitable?

Just enter your data and let The Business Plan Shop crunch the numbers. We will tell if your business idea can generate profits and cash flows, and how much you need to get started.

Build your insurance brokerage firm's financial forecast

The next step to start your insurance brokerage firm: putting your financial projections together.

What is the financial forecast for an insurance brokerage firm?

A forecast is a quantified decision-making document that shows the initial investment required to open an insurance brokerage firm and the company's potential profitability and cash flow generation over the next 3 to 5 years.

As you think about your insurance brokerage firm idea, the main role of financial projections will be to help you decide whether it makes sense to create the company.

Building a financial forecast helps determine the amount of initial financing required to start your insurance brokerage firm.

In fact, creating financial projections is the only way to assess the amount of initial financing you'll need to open your insurance brokerage firm, and to make sure your project makes economic and financial sense.

Keep in mind that very few business ideas are financially viable. At The Business Plan Shop, we've seen nearly a million business start-up ideas, and we estimate that less than one in four is economically viable.

Your forecast will therefore require your full attention and constant revision, as your project matures. It's also a good idea to simulate different scenarios to anticipate several possibilities (what happens if your sales take longer than expected to ramp up, for example), so you're ready for all eventualities.

When seeking financing, your forecast will be incorporated into your business plan, which is the document you will use to present your business idea to financial partners. We'll come back to the business plan in more detail later in this guide.

Creating and updating your insurance brokerage firm's forecast is an ongoing process. Indeed, having up-to-date financial projections is the only way to maintain visibility over your company's future cash flow and cash position.

Forecasting is, therefore, the financial management tool that will be with you throughout the life of your company. Once you've started trading, you'll need to regularly compare the difference between your actual accounts and your forecasts, and then adjust them to maintain visibility over your future cash flows.

What does a financial forecast look like?

Once ready, your insurance brokerage firm forecast will be presented using the financial tables below.

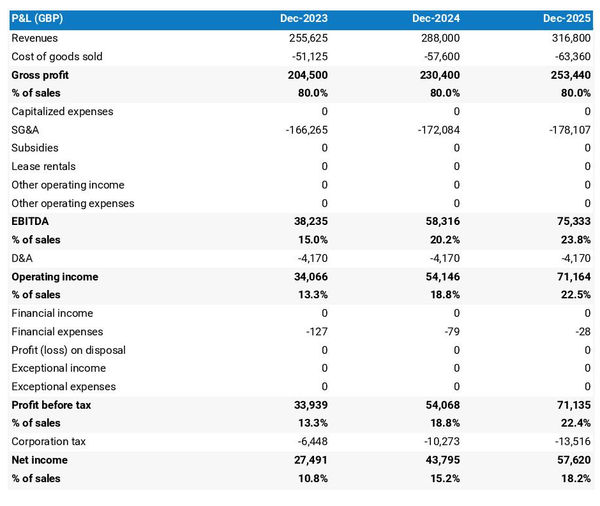

The forecasted profit & loss statement

The profit & loss forecast gives you a clear picture of your business’ expected growth over the first three to five years, and whether it’s likely to be profitable or not.

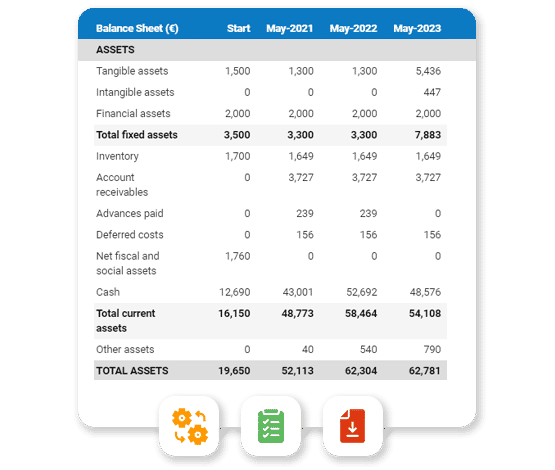

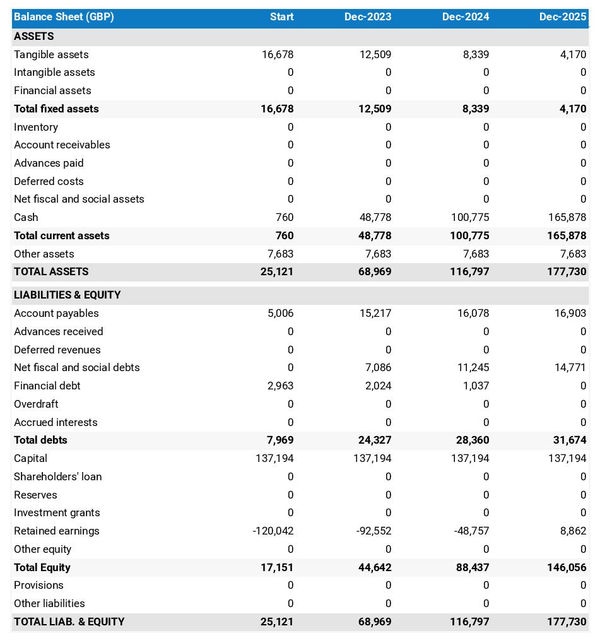

The projected balance sheet

Your insurance brokerage firm's forecasted balance sheet enables you to assess your financial structure and working capital requirements.

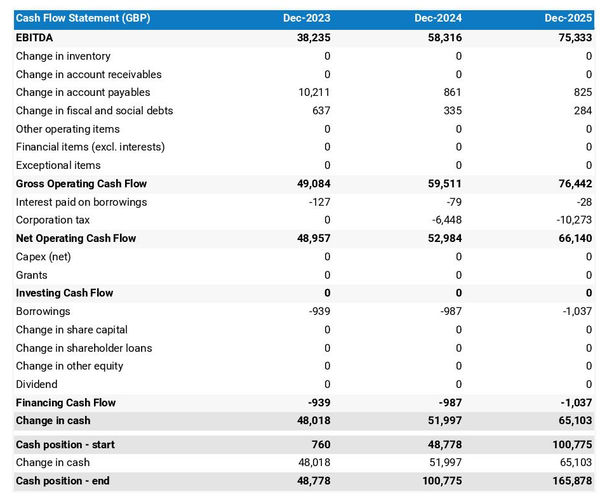

The projected cash flow statement

A projected cash flow statement to start an insurance brokerage firm is used to show how much cash the business is expected to generate or consume over the first three years.

Which solution should you use to make a financial projection for your insurance brokerage firm?

Using an online financial forecasting tool, such as the one we offer at The Business Plan Shop, is the simplest and safest solution for forecasting your insurance brokerage firm.

There are several advantages to using specialised software:

- You can easily create your financial forecast by letting the software take care of the financial calculations for you without errors

- You have access to complete financial forecast templates

- You get a complete financial forecast ready to be sent to your bank or investors

- The software helps you identify and correct any inconsistencies in your figures

- You can create scenarios to stress-test your forecast's main assumptions to stress-test the robustness of your business model

- After you start trading, you can easily track your actual financial performance against your financial forecast, and recalibrate your forecast to maintain visibility on your future cash flows

- You have a friendly support team on standby to assist you when you are stuck

If you are interested in this type of solution, you can try our forecasting software for free by signing up here.

Choose a name and register your insurance brokerage firm

The next phase in launching your insurance brokerage firm involves selecting a name for your company.

This stage is trickier than it seems. Finding the name itself is quite fun; the difficulty lies in finding one that is available and being the first to reserve it.

You cannot take a name that is similar to a name already used by a competitor or protected by a registered trademark without inevitably risking legal action.

So you need to find a name that is available, and be able to register it before someone else can.

In addition, you will probably want to use the same name for:

- Your company’s legal name - Example LTD

- Your business trading name - Example

- The trademark - Example ®

- Your company’s domain name - Example.com

The problem is that the procedures for registering these different names are carried out in different places, each with their own deadlines:

- Registering a domain name takes only a few minutes

- Registering a new trademark takes at least 12 weeks (if your application is accepted)

- The time taken to register a new business depends on the country, but it's generally fast

You will therefore be faced with the choice of: either registering everything at once and hoping that your name will be accepted everywhere, or proceeding step by step in order to minimise costs, but taking the risk that someone else will register one of the names you wanted in the meantime.

Our advice is to discuss strategy with your legal counsel (see further down in this guide) and prioritise your domain names and registered trademarks. You'll always have the option of using a trade name that's different from your company's legal name, and that's not a big deal.

To check that the name you want is not already in use, you should consult:

- Your country's business register

- The relevant trademark registers depending on which countries you want to register your trade mark in

- A domain name reservation company such as GoDaddy

- An Internet search engine

In this area too, your legal counsel will be able to help with the research and formalities.

Need inspiration for your business plan?

Avoid writer's block and draft your own business plan in no time by drawing inspiration from dozens of business plan templates.

Deciding upon the corporate identity of your insurance brokerage firm

The next step in opening an insurance brokerage firm is to look at your company's visual identity.

Your company's “visual identity” plays a crucial role in shaping your brand image. It helps you to be recognizable and to stand out from your competitors.

Although you can define your visual identity yourself, it is generally advisable to call on the services of a designer or marketing agency to achieve a professional result.

At a minimum, you will need to define the following elements:

- Logo

- Brand guidelines

- Business cards

- Website theme

Logo

Your insurance brokerage firm's logo allows others to quickly identify your company. It will be used on all your communication media (website, social networks, business cards, etc.) and official documents (invoices, contracts, etc.).

In addition to its design, it's important that your logo is available in a variety of colors, so that it can be seen on all media (white, dark background, etc.).

Brand guidelines

Having brand guidelines enables you to maintain consistency in formatting across all your communications media and official documents.

Brand guidelines define the font (family and size), design and colours used by your brand.

In terms of fonts, for example, you may use Roboto in size 20 for your titles and Lato in size 14 for your texts.

The colours used to represent your brand should generally be limited to five:

- The main colour,

- A secondary colour (the accent),

- A dark background colour (blue or black),

- A grey background colour (to vary from white),

- Possibly another secondary colour.

Business cards

Designing business cards for your insurance brokerage firm is a must, as they will allow you to communicate your contact details to your customers, suppliers, partners, potential recruits, etc.

In principle, they will include your logo and the brand guidelines that we mentioned above.

Website theme

In the same way, the theme of your insurance brokerage firm website will be based on your logo and the brand guidelines we mentioned above.

This involves defining the look and feel of your site's main graphic elements:

- Buttons,

- Menus,

- Forms,

- Banners,

- Etc.

Navigate the legal and regulatory requirements for launching your insurance brokerage firm

The next thing to do in getting an insurance brokerage firm off the ground is to handle all the legal and regulatory requirements. We recommend that you be accompanied by a law firm for all of the steps outlined below.

Intellectual property

One of your priorities will be to ensure that your company's intellectual property is adequately protected.

As explained before, you can choose to register a trademark. Your lawyer can help you with a detailed search to make sure your chosen trademark is unique and doesn't clash with existing ones.

They'll assist in preparing the required documents and steer you in picking the right categories and locations for trademark registration.

Moreover, your lawyer can offer guidance on additional measures to protect other intellectual property assets your company may have.

Getting your insurance brokerage firm paperwork in order

For day-to-day operations, your insurance brokerage firm will need to rely on a set of contractual documents.

Your exact needs in this respect will depend on the country in which you are launching your insurance brokerage firm, the number of partners and the envisaged size of the company.

However, you will probably need at least the following documents:

- Employment contracts

- General terms and conditions of sale

- General terms and conditions of use for your website

- Privacy Policy for your website

- Cookie Policy for your website

- Invoices

- Etc.

Applying for licences and permits and registering for various taxes

Operating your business legally may require licences and business permits. The exact requirements applicable to your situation will depend on the country in which you set up your insurance brokerage firm.

The lawyers who advise you will also be able to guide you with regard to all the rules applicable to your business.

Similarly, your accountant will be able to help you take the necessary steps to comply with the tax authorities.

Need a convincing business plan?

The Business Plan Shop makes it easy to create a financial forecast and write a business plan to help convince investors that your business idea can be profitable.

Create a business plan for your insurance brokerage firm

The next step to open an insurance brokerage firm: put together your business plan.

What is a business plan?

To keep it simple, a business plan comprises two crucial components:

- Firstly, a numerical part, the financial forecast (which we mentioned earlier), which highlights the initial financing requirements and profitability potential of the insurance brokerage firm,

- And a written, well-argued section that presents your project in detail, aims to convince the reader of its chances of success, and provides the context needed to assess whether the forecast is realistic or not.

The business plan will enable you to verify the coherence of your project, and ensure that the company can be profitable before incurring further costs. It will also help you convince business and financial partners.

As you can see, your business plan must be convincing and error-free.

How to write a business plan for an insurance brokerage firm?

Nowadays, the modern and most efficient way to write an insurance brokerage firm business plan is to use startup business plan software like the one we offer at The Business Plan Shop.

Using The Business Plan Shop to create a business plan for aninsurance brokerage firm has several advantages :

- You can easily create your financial forecast by letting the software take care of the financial calculations for you without errors

- You are guided through the writing process by detailed instructions and examples for each part of the plan

- You can access a library of dozens of complete startup business plan samples and templates for inspiration

- You get a professional business plan, formatted and ready to be sent to your bank or investors

- You can create scenarios to stress test your forecast's main assumptions

- You can easily track your actual financial performance against your financial forecast by importing accounting data

- You can easily update your forecast as time goes by to maintain visibility on future cash flows

- You have a friendly support team on standby to assist you when you are stuck

If you're interested in using this type of solution, you can try The Business Plan Shop for free by signing up here.

Need a convincing business plan?

The Business Plan Shop makes it easy to create a financial forecast and write a business plan to help convince investors that your business idea can be profitable.

Raise the financing needed to launch your insurance brokerage firm

With your business plan in hand, you can tackle one of the final steps to open an insurance brokerage firm business: the search for financing.

Raising the capital needed to launch your business will probably require a combination of equity and debt, which are the two types of financing available to companies.

Equity funding

Equity is the sum of money invested in an insurance brokerage firm by both founders and investors.

Equity is a key factor in business start-ups. Should the project fail, the sums invested in equity are likely to be lost; these sums therefore enable the founders to send a strong signal to their commercial and financial partners as to their conviction in the project's chances of success.

In terms of return on investment, equity investors can either receive dividends from the company (provided it is profitable) or realize capital gains by selling their shares (provided a buyer is interested in the company).

Equity providers are therefore in a very risky position. They can lose everything in the event of bankruptcy, and will only see a return on their investment if the company is profitable or resold. On the other hand, they can generate a very high return if the project is a success.

Given their position, equity investors look for start-up projects with sufficient growth and profitability potential to offset their risk.

From a technical standpoint, equity includes:

- Share capital and premiums: which represent the amount invested by the shareholders. This capital is considered permanent as it is non-refundable. In return for their investment, shareholders receive shares that entitle them to information, decision-making power (voting in general assembly), and the potential to receive a portion of any dividends distributed by the company.

- Director loans: these are examples of non-permanent capital advanced to the company by the shareholders. This is a more flexible way of injecting some liquidity into your company as you can repay director loans at any time.

- Reserves: these represent the share of profits set aside to strengthen the company's equity. Allocating a percentage of your profits to the reserves can be mandatory in certain cases (legal or statutory requirement depending on the legal form of your company). Once allocated in reserves, these profits can no longer be distributed as dividends.

- Investment grants: which represent any non-refundable amounts received by the company to help it invest in long-term assets.

- Other equity: which includes the equity items which don't fit in the other categories. Mostly convertible or derivative instruments. For a small business, it is likely that you won't have any other equity items.

The main sources of equity are as follows:

- Contributions made by the owners.

- Private investors: business angels, friends and family.

- Crowdfunding: raising funds by involving a group of people through campaigns where they contribute money or make donations, often getting something in return for their support.

- Start-up aid, e.g. government loans to help founders build up their start-up capital.

Debt financing

Debt is the other way of financing companies. Unlike equity, debt offers lenders a limited, contractually guaranteed return on their investment.

Your insurance brokerage firm undertakes to pay lenders' interest and repay the capital borrowed according to a pre-agreed schedule. Lenders are therefore making money whether or not your company makes a profit.

As a result, the only risk lenders take is that of your insurance brokerage firm going bankrupt, so they're extremely conservative and will want to see prudent, hands-on management of the company's finances.

From the point of view of the company and all its stakeholders (workforce, customers, suppliers, etc.), the company's contractual obligation to repay lenders increases the risk for all. As a result, there is a certain caution towards companies which are too heavily indebted.

Businesses can borrow debt in two main ways:

- Against assets: this is the most common way of borrowing. The bank funds a percentage of the price of an asset (a vehicle or a building, for example) and takes the asset as collateral. If the business cannot repay the loan, the bank takes the asset and sells it to reduce losses.

- Against cash flows: the bank looks at how much profit and cash flow the business expects to make in the future. Based on these projections, it assigns a credit risk to the business and decides how much the business can borrow and under what terms (amount, interest rate, and duration of the loan).

It's difficult to borrow against future cash flows when you're starting an insurance brokerage firm, because the business doesn't yet have historical data to reassure about the credibility of cash flow forecast.

Borrowing to finance a portion of equipment purchases is therefore often the only option available to founders. The assets that can be financed with this option must also be easy to resell, in the unfortunate event that the bank is forced to seize them, which could limit your options even further.

As far as possible sources of borrowing are concerned, the main ones here are banks and credit institutions. Bear in mind, however, that each institution is different, in terms of the risk it is prepared to accept, what it is willing to finance, and how the risk of your project will be perceived.

In some countries, it is also possible to borrow from private investors (directly or via crowdfunding platforms) or other companies, but not everywhere.

Key points about financing your insurance brokerage firm

Multiple solutions are available to help you raise the initial financing you need to open your insurance brokerage firm. A minimum amount of equity will be needed to give the project credibility, and bank financing can be sought to complete the financing.

Track your actuals against your forecast

You've reached the end of the road and are ready to launch your insurance brokerage firm.

Congratulations and welcome to the fantastic world of entrepreneurship! Celebrate the work you've done so far, and get back to work quickly, because this is where the real work begins.

Your first priority will be to do everything you can to make your business sustainable (and thus avoid being one of the 50% of start-ups that fail within five years of launching).

Your business plan will be your best ally to ensure that you're on track to achieve your objectives, or to help rectify the situation if necessary.

The key to financial management is to regularly compare your actual accounting data with your insurance brokerage firm forecasts, in order to be able to :

- Quantify the gaps between what you planned and what you achieved

- Adjust your financial forecasts as the year progresses to maintain visibility over your future cash flow

No one can predict the future with certainty, but by closely monitoring the variances between actuals and forecasts, regularly adjusting your forecasts and simulating several scenarios, you can prepare your insurance brokerage firm for the worst while hoping for the best.

It's the only way to keep an eye on your cash flow and actively manage the development of your insurance brokerage firm, ultimately reducing the risk to your company.

There's nothing worse than waiting for your company's annual accounts to close, which can be many months after the end of your financial year (up to nine months in the UK for example), only to realize that you've fallen far short of your forecasts for the past year, and that your insurance brokerage firm urgently needs a cash injection to keep going.

That's why it's strongly recommended to use a financial planning and analysis solution that integrates forecasting, scenario analysis, and actuals vs. forecast tracking, like we do at The Business Plan Shop with our financial dashboards.

Need inspiration for your business plan?

Avoid writer's block and draft your own business plan in no time by drawing inspiration from dozens of business plan templates.

Key takeaways

- To open an insurance brokerage firm you need to go through each of the 15 steps we have outlined in this guide.

- The financial forecast is the tool that will enable you to check that your project can be profitable and to estimate the investment and initial financing requirements.

- The business plan is the document that your financial partners will ask you to produce when seeking finance.

- Once you have started trading, it will be essential to keep your financial forecasts up to date in order to maintain visibility of the future cash flow of your insurance brokerage firm.

- Leveraging a financial planning and analysis platform that seamlessly integrates forecasts, business plans, and real-time performance monitoring — like The Business Plan Shop — simplifies the process and mitigates risks associated with launching a business.

We hope this practical guide has given you a better understanding of how to open an insurance brokerage firm. Please do not hesitate to contact our team if you have any questions or if you would like to share your experience of setting up your own business.

Also on The Business Plan Shop

Do you know someone who is thinking about opening an insurance brokerage firm? Share our guide with them!

Founder & CEO at The Business Plan Shop Ltd