How to write a business plan for an insurance broker?

Creating a business plan for an insurance broker is an essential process for any entrepreneur. It serves as a roadmap that outlines the necessary steps to be taken to start or grow the business, the resources required, and the anticipated financial outcomes. It should be crafted with method and confidence.

This guide is designed to provide you with the tools and knowledge necessary for creating an insurance broker business plan, covering why it is so important both when starting up and running an established business, what should be included in your plan, how it should be structured, what tools should be used to save time and avoid errors, and other helpful tips.

We have a lot to cover, so let's get to it!

Why write a business plan for an insurance broker?

Being clear on the scope and goals of the document will make it easier to understand its structure and content. So before diving into the actual content of the plan, let's have a quick look at the main reasons why you would want to write an insurance broker business plan in the first place.

To have a clear roadmap to grow the business

Running a small business is tough! Economic cycles bring growth and recessions, while the business landscape is ever-changing with new technologies, regulations, competitors, and consumer behaviours emerging constantly.

In such a dynamic context, operating a business without a clear roadmap is akin to driving blindfolded: it's risky, to say the least. That's why crafting a business plan for your insurance broker is vital to establish a successful and sustainable venture.

To create an effective business plan, you'll need to assess your current position (if you're already in business) and define where you want the business to be in the next three to five years.

Once you have a clear destination for your insurance broker, you'll have to:

- Identify the necessary resources (human, equipment, and capital) needed to reach your goals,

- Determine the pace at which the business needs to progress to meet its objectives as scheduled,

- Recognize and address the potential risks you may encounter along the way.

Engaging in this process regularly proves advantageous for both startups and established companies. It empowers you to make informed decisions about resource allocation, ensuring the long-term success of your business.

To get visibility on future cash flows

If your small insurance broker runs out of cash: it's game over. That's why we often say "cash is king", and it's crucial to have a clear view of your insurance broker's future cash flows.

So, how can you achieve this? It's simple - you need to have an up-to-date financial forecast.

The good news is that your insurance broker business plan already includes a financial forecast (which we'll discuss further in this guide). Your task is to ensure it stays current.

To accomplish this, it's essential to regularly compare your actual financial performance with what was planned in your financial forecast. Based on your business's current trajectory, you can make adjustments to the forecast.

By diligently monitoring your insurance broker's financial health, you'll be able to spot potential financial issues, like unexpected cash shortfalls, early on and take corrective actions. Moreover, this practice will enable you to recognize and capitalize on growth opportunities, such as excess cash flow enabling you to expand to new locations.

To secure financing

Whether you are a startup or an existing business, writing a detailed insurance broker business plan is essential when seeking financing from banks or investors.

This makes sense given what we've just seen: financiers want to ensure you have a clear roadmap and visibility on your future cash flows.

Banks will use the information included in the plan to assess your borrowing capacity (how much debt your business can support) and your ability to repay the loan before deciding whether they will extend credit to your business and on what terms.

Similarly, investors will review your plan carefully to assess if their investment can generate an attractive return on investment.

To do so, they will be looking for evidence that your insurance broker has the potential for healthy growth, profitability, and cash flow generation over time.

Now that you understand why it is important to create a business plan for an insurance broker, let's take a look at what information is needed to create one.

Need a convincing business plan?

The Business Plan Shop makes it easy to create a financial forecast to assess the potential profitability of your projects, and write a business plan that’ll wow investors.

Information needed to create a business plan for an insurance broker

Drafting an insurance broker business plan requires research so that you can project sales, investments and cost accurately in your financial forecast, and convince the reader that there is a viable commercial opportunity to be seized.

Below, we'll focus on three critical pieces of information you should gather before starting to write your plan.

Carrying out market research for an insurance broker

Before you begin writing your business plan for an insurance broker, conducting market research is a critical step in ensuring precise and realistic financial projections.

Market research grants you valuable insights into your target customer base, competitors, pricing strategies, and other crucial factors that can impact the success of your business.

In the course of this research, you may stumble upon trends that could impact your insurance broker.

Your market research might reveal that customers may be more likely to select insurance plans with additional coverage options, such as pet insurance or identity theft coverage. It could also indicate that there may be a growing demand for digital insurance services, like online payment systems or automated customer support.

Such market trends play a pivotal role in revenue forecasting, as they provide essential data regarding potential customers' spending habits and preferences.

By integrating these findings into your financial projections, you can provide investors with more accurate information, enabling them to make well-informed decisions about investing in your insurance broker.

Developing the sales and marketing plan for an insurance broker

As you embark on creating your insurance broker business plan, it is crucial to budget sales and marketing expenses beforehand.

A well-defined sales and marketing plan should include precise projections of the actions required to acquire and retain customers. It will also outline the necessary workforce to execute these initiatives and the budget required for promotions, advertising, and other marketing efforts.

This approach ensures that the appropriate amount of resources is allocated to these activities, aligning with the sales and growth objectives outlined in your business plan.

The staffing and equipment needs of an insurance broker

As you embark on starting or expanding your insurance broker, having a clear plan for recruitment and capital expenditures (investment in equipment and real estate) is essential for ensuring your business's success.

Both the recruitment and investment plans must align with the timing and level of growth projected in your forecast, and they require appropriate funding.

The staffing costs for an insurance broker might include salaries for a team of insurance agents, administrative staff, and customer service personnel.

Additionally, your insurance broker might also need to pay for additional staffing costs such as training, benefits, and payroll taxes. The equipment costs for an insurance broker might include computers, software, printers, scanners, and other office supplies.

Your broker may also need to purchase specialized equipment such as laptops, tablets, and mobile phones in order to provide the best customer service. Finally, your broker may need to pay for additional costs such as internet access, phone lines, and other office expenses.

To create a realistic financial forecast, you also need to consider other operating expenses associated with the day-to-day running of your business, such as insurance and bookkeeping.

With all the necessary information at hand, you are ready to begin crafting your business plan and developing your financial forecast.

What goes into your insurance broker's financial forecast?

The financial forecast of your insurance broker will enable you to assess the profitability potential of your business in the coming years and how much capital is required to fund the actions planned in the business plan.

The four key outputs of a financial forecast for a insurance broker are:

- The profit and loss (P&L) statement,

- The projected balance sheet,

- The cash flow forecast,

- And the sources and uses table.

Let's take a closer look at each of these.

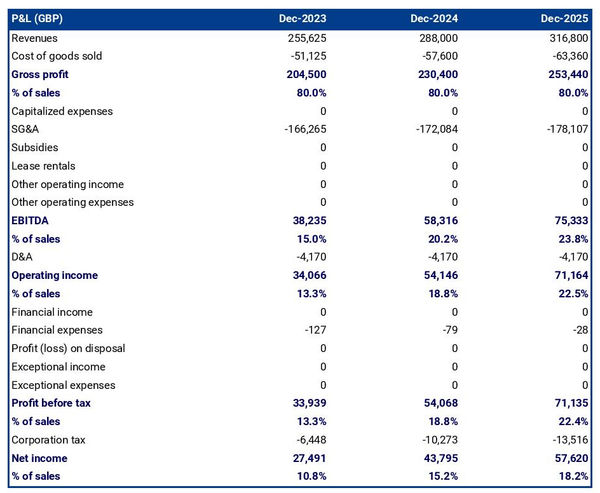

The projected P&L statement

Your insurance broker forecasted P&L statement enables the reader of your business plan to get an idea of how much revenue and profits your business is expected to make in the near future.

Ideally, your reader will want to see:

- Growth above the inflation level

- Expanding profit margins

- Positive net profit throughout the plan

Expectations for an established insurance broker will of course be different than for a startup. Existing businesses which have reached their cruising altitude might have slower growth and higher margins than ventures just being started.

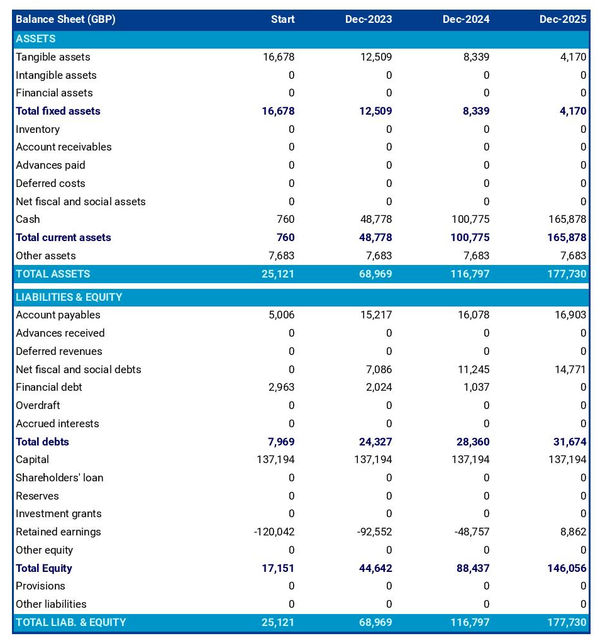

The forecasted balance sheet of your insurance broker

The projected balance sheet of your insurance broker will enable the reader of your business plan to assess the overall financial health of your business.

It shows three elements: assets, liabilities and equity:

- Assets: are productive resources owned by the business, such as equipment, cash, and accounts receivable (money owed by clients).

- Liabilities: are debts owed to creditors, lenders, and other entities, such as accounts payable (money owed to suppliers).

- Equity: includes the sums invested by the shareholders or business owners and the profits and losses accumulated by the business to date (which are called retained earnings). It is a proxy for the value of the owner's stake in the business.

Analysing your insurance broker projected balance sheet provides an understanding of your insurance broker's working capital structure, investment and financing policies.

In particular, the readers of your plan can compare the level of financial debt on the balance sheet to the equity value to measure the level of financial risk (equity doesn't need to be reimbursed, while financial debt must be repaid, making it riskier).

They can also use your balance sheet to assess your insurance broker's liquidity and solvency:

- A liquidity analysis: focuses on whether or not your business has sufficient cash and short-term assets to cover its liabilities due in the next 12 months.

- A solvency analysis: takes and longer view to assess whether or not your business has the capacity to repay its debts over the medium-term.

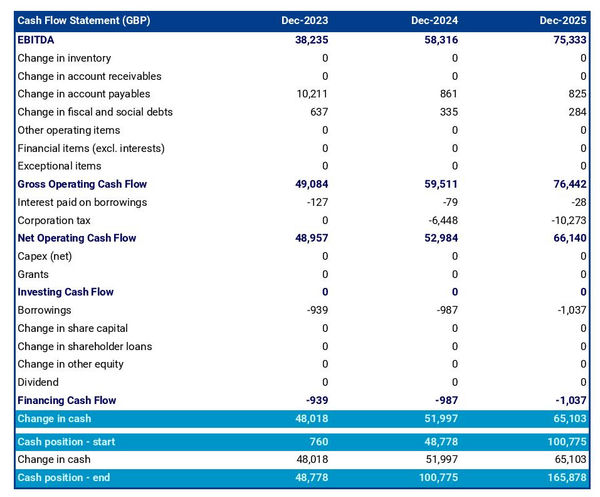

The cash flow forecast

As we've seen earlier in this guide, monitoring future cash flows is the key to success and the only way of ensuring that your insurance broker has enough cash to operate.

As you can expect showing future cash flows is the main role of the cash flow forecast in your insurance broker business plan.

It is best practice to organise the cash flow statement by nature in order to show the cash impact of the following areas:

- Cash flow generated from operations: the operating cash flow shows how much cash is generated or consumed by the business's commercial activities

- Cash flow from investing activities: the investing cash flow shows how much cash is being invested in capital expenditure (equipment, real estate, etc.) either to maintain the business's equipment or to expand its capabilities

- Cash flow from financing activities: the financing cash flow shows how much cash is raised or distributed to financiers

Looking at the cash flow forecast helps you to make sure that your business has enough cash to keep running, and can help you anticipate potential cash shortfalls.

Your insurance broker business plan will normally include both yearly and monthly cash flow forecasts so that the readers can view the impact of seasonality on your business cash position and generation.

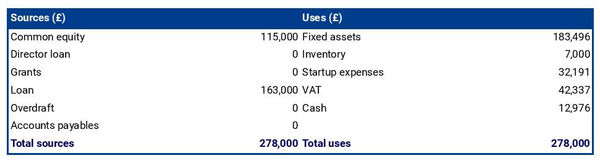

The initial financing plan

The initial financing plan - also called a sources and uses table - is an important tool when starting an insurance broker.

It shows where the money needed to set up the business will come from (sources) and how it will be allocated (uses).

Having this table helps understand what costs are involved in setting up the insurance broker, how the risks are distributed between the shareholders and the lenders, and what will be the starting cash position (which needs to be sufficient to sustain operations until the business breaks even).

Now that the financial forecast of an insurance broker business plan is understood, let's focus on what goes into the written part of the plan.

Need a convincing business plan?

The Business Plan Shop makes it easy to create a financial forecast to assess the potential profitability of your projects, and write a business plan that’ll wow investors.

The written part of an insurance broker business plan

The written part of an insurance broker business plan plays a key role: it lays out the plan of action you intend to execute to seize the commercial opportunity you've identified on the market and provides the context needed for the reader to decide if they believe your plan to be achievable and your financial forecast to be realistic.

The written part of an insurance broker business plan is composed of 7 main sections:

- The executive summary

- The presentation of the company

- The products and services

- The market analysis

- The strategy

- The operations

- The financial plan

Let's go through the content of each section in more detail!

1. The executive summary

The executive summary, the first section of your insurance broker's business plan, serves as an inviting snapshot of your entire plan, leaving readers eager to know more about your business.

To compose an effective executive summary, start with a concise introduction of your business, covering its name, concept, location, history, and unique aspects. Share insights about the services or products you intend to offer and your target customer base.

Subsequently, provide an overview of your insurance broker's addressable market, highlighting current trends and potential growth opportunities.

Then, present a summary of critical financial figures, such as projected revenues, profits, and cash flows.

You should then include a summary of your key financial figures such as projected revenues, profits, and cash flows.

Lastly, address any funding needs in the "ask" section of your executive summary.

2. The presentation of the company

In your insurance broker business plan, the second section should focus on the structure and ownership, location, and management team of your company.

In the structure and ownership part, you'll provide an overview of the business's legal structure, details about the owners, and their respective investments and ownership shares. This clarity is crucial, especially if you're seeking financing, as it helps the reader understand which legal entity will receive the funds and who controls the business.

Moving on to the location part, you'll offer an overview of the company's premises and their surroundings. Explain why this particular location is of interest, highlighting factors like catchment area, accessibility, and nearby amenities.

When describing the location of your insurance broker, you could emphasize the potential for growth in the area. You may discuss the fact that there are plenty of resources and opportunities in the surrounding area that could help to increase the profitability of the business. Additionally, you could point out that the area could potentially provide access to a wider customer base, allowing for greater success in the future.

Finally, you should introduce your management team. Describe each member's role, background, and experience.

Don't forget to emphasize any past successes achieved by the management team and how long they've been working together. Demonstrating their track record and teamwork will help potential lenders or investors gain confidence in their leadership and ability to execute the business plan.

3. The products and services section

The products and services section of your business plan should include a detailed description of what your company offers, who are the target customers, and what distribution channels are part of your go-to-market.

For example, your insurance broker might offer auto insurance for customers needing coverage for personal vehicles, home insurance for customers needing coverage for their homes, and business insurance for customers needing coverage for their businesses.

These products and services can provide customers with financial protection against unexpected events such as theft, property damage, and liability claims.

4. The market analysis

When outlining your market analysis in the insurance broker business plan, it's essential to include comprehensive details about customers' demographics and segmentation, target market, competition, barriers to entry, and relevant regulations.

The primary aim of this section is to give the reader an understanding of the market size and appeal while demonstrating your expertise in the industry.

To begin, delve into the demographics and segmentation subsection, providing an overview of the addressable market for your insurance broker, key marketplace trends, and introducing various customer segments and their preferences in terms of purchasing habits and budgets.

Next, shift your focus to the target market subsection, where you can zoom in on the specific customer segments your insurance broker targets. Explain how your products and services are tailored to meet the unique needs of these customers.

For example, your target market might include young married couples. This segment is likely to be looking for a comprehensive insurance plan that offers good value for money. They are likely to be tech savvy and looking to do research online and compare prices.

In the competition subsection, introduce your main competitors and explain what sets your insurance broker apart from them.

Finally, round off your market analysis by providing an overview of the main regulations that apply to your insurance broker.

5. The strategy section

When crafting the strategy section of your business plan for your insurance broker, it's important to cover several key aspects, including your competitive edge, pricing strategy, sales & marketing plan, milestones, and risks and mitigants.

In the competitive edge subsection, clearly explain what sets your company apart from competitors. This is particularly critical if you're a startup, as you'll be trying to establish your presence in the marketplace among entrenched players.

The pricing strategy subsection should demonstrate how you aim to maintain profitability while offering competitive prices to your customers.

For the sales & marketing plan, outline how you plan to reach and acquire new customers, as well as retain existing ones through loyalty programs or special offers.

In the milestones subsection, detail what your company has achieved thus far and outline your primary objectives for the coming years by including specific dates for expected progress. This ensures everyone involved has clear expectations.

Lastly, in the risks and mitigants subsection, list the main risks that could potentially impact the execution of your plan. Explain the measures you've taken to minimize these risks. This is vital for investors or lenders to feel confident in supporting your venture - try to proactively address any objection they might have.

Your insurance broker may face the risk of a client making a fraudulent claim. This could lead to a costly investigation and the broker may face legal and financial repercussions.

Additionally, the broker may face the risk of a cyber attack that could lead to the exposure of sensitive information. This could result in a loss of trust from customers and a damaged reputation.

6. The operations section

The operations of your insurance broker must be presented in detail in your business plan.

The first thing you should cover in this section is your staffing team, the main roles, and the overall recruitment plan to support the growth expected in your business plan. You should also outline the qualifications and experience necessary to fulfil each role, and how you intend to recruit (using job boards, referrals, or headhunters).

You should then state the operating hours of your insurance broker - so that the reader can check the adequacy of your staffing levels - and any plans for varying opening times during peak season. Additionally, the plan should include details on how you will handle customer queries outside of normal operating hours.

The next part of this section should focus on the key assets and IP required to operate your business. If you depend on any licenses or trademarks, physical structures (equipment or property) or lease agreements, these should all go in there.

You may have key assets such as customer databases and client records that could contain sensitive information. Additionally, your insurance broker might have intellectual property such as proprietary knowledge or business processes that could be valuable to the company.

Finally, you should include a list of suppliers that you plan to work with and a breakdown of their services and main commercial terms (price, payment terms, contract duration, etc.). Investors are always keen to know if there is a particular reason why you have chosen to work with a specific supplier (higher-quality products or past relationships for example).

7. The presentation of the financial plan

The financial plan section is where we will present the financial forecast we talked about earlier in this guide.

Now that you have a clear idea of what goes in your insurance broker business plan, let's look at the solutions you can use to draft yours.

What tool should I use to write my insurance broker's business plan?

In this section, we will be reviewing the two main solutions for creating an insurance broker business plan:

- Using specialized online business plan software,

- Outsourcing the plan to the business plan writer.

Using an online business plan software for your insurance broker's business plan

The modern and most efficient way to write an insurance broker business plan is to use business plan software.

There are several advantages to using specialized software:

- You can easily create your financial forecast by letting the software take care of the financial calculations for you without errors

- You are guided through the writing process by detailed instructions and examples for each part of the plan

- You can access a library of dozens of complete business plan samples and templates for inspiration

- You get a professional business plan, formatted and ready to be sent to your bank or investors

- You can easily track your actual financial performance against your financial forecast

- You can create scenarios to stress test your forecast's main assumptions

- You can easily update your forecast as time goes by to maintain visibility on future cash flows

- You have a friendly support team on standby to assist you when you are stuck

If you're interested in using this type of solution, you can try The Business Plan Shop for free by signing up here.

Need a convincing business plan?

The Business Plan Shop makes it easy to create a financial forecast to assess the potential profitability of your projects, and write a business plan that’ll wow investors.

Hiring a business plan writer to write your insurance broker's business plan

Outsourcing your insurance broker business plan to a business plan writer can also be a viable option.

Business plan writers are skilled in creating error-free business plans and accurate financial forecasts. Moreover, hiring a consultant can save you valuable time, allowing you to focus on day-to-day business operations.

However, it's essential to be aware that hiring business plan writers will be expensive, as you're not only paying for their time but also the software they use and their profit margin.

Based on experience, you should budget at least £1.5k ($2.0k) excluding tax for a comprehensive business plan, and more if you require changes after initial discussions with lenders or investors.

Also, exercise caution when seeking investment. Investors prefer their funds to be directed towards business growth rather than spent on consulting fees. Therefore, the amount you spend on business plan writing services and other consulting services should be insignificant compared to the amount raised.

Keep in mind that one drawback is that you usually don't own the business plan itself; you only receive the output, while the actual document is saved in the consultant's business planning software. This can make it challenging to update the document without retaining the consultant's services.

For these reasons, carefully consider outsourcing your insurance broker business plan to a business plan writer, weighing the advantages and disadvantages of seeking outside assistance.

Why not create your insurance broker's business plan using Word or Excel?

I must advise against using Microsoft Excel and Word (or their Google, Apple, or open-source equivalents) to write your insurance broker business plan. Let me explain why.

Firstly, creating an accurate and error-free financial forecast on Excel (or any spreadsheet) is highly technical and requires a strong grasp of accounting principles and financial modelling skills. It is, therefore, unlikely that anyone will fully trust your numbers unless you have both a degree in finance and accounting and significant financial modelling experience, like us at The Business Plan Shop.

Secondly, relying on spreadsheets is inefficient. While it may have been the only option in the past, technology has advanced significantly, and software can now perform these tasks much faster and with greater accuracy. With the rise of AI, software can even help us detect mistakes in forecasts and analyze the numbers for better decision-making.

And with the rise of AI, software is also becoming smarter at helping us detect mistakes in our forecasts and helping us analyse the numbers to make better decisions.

Moreover, software makes it easier to compare actuals versus forecasts and maintain up-to-date forecasts to keep visibility on future cash flows, as we discussed earlier in this guide. This task is cumbersome when using spreadsheets.

Now, let's talk about the written part of your insurance broker business plan. While it may be less error-prone, using software can bring tremendous gains in productivity. Word processors, for example, lack instructions and examples for each part of your business plan. They also won't automatically update your numbers when changes occur in your forecast, and they don't handle formatting for you.

Overall, while Word or Excel may seem viable for some entrepreneurs to create a business plan, it's by far becoming an antiquated way of doing things.

Takeaways

- A business plan has 2 complementary parts: a financial forecast showcasing the expected growth, profits and cash flows of the business; and a written part which provides the context needed to judge if the forecast is realistic and relevant.

- Having an up-to-date business plan is the only way to keep visibility on your insurance broker's future cash flows.

- Using business plan software is the modern way of writing and maintaining business plans.

We hope that this practical guide gave you insights on how to write the business plan for your insurance broker. Do not hesitate to get in touch with our team if you still have questions.

Also on The Business Plan Shop

- In-depth business plan structure

- How to write the business plan for a grant application?

- Difference between business case and business plan

- Difference between business plan and budget

- Key steps to write a business plan?

- Free business plan template

Know someone who owns or wants to start an insurance broker? Share this article with them!

Founder & CEO at The Business Plan Shop Ltd