How to open an oyster farm?

Want to start an oyster farm but don't know where to begin? Then you've come to the right place!

Our comprehensive guide covers everything related to opening an oyster farm - from choosing the right concept to setting out your marketing plan and financing your business.

You'll also learn how to assess the profitability of your business idea and decide whether or not it can be viable from a financial perspective.

Ready to kickstart your entrepreneurial journey? Let's begin!

What is the business model of an oyster farm?

Before thinking about starting an oyster farm, you'll need to have a solid understanding of its business model (how it generates profits) and how the business operates on a daily basis.

Doing so will help you decide whether or not this is the right business idea for you, given your skillset, personal savings, and lifestyle choices.

Looking at the business model in detail will also enable you to form an initial view of the potential for growth and profitability, and to check that it matches your level of ambition.

The easiest ways to acquire insights into how an oyster farm works are to:

- Speak with oyster farm owners

- Undertake work experience with a successful oyster farm

- Participate in a training course

Speak with oyster farm owners

Talking to seasoned entrepreneurs who have also set up an oyster farm will enable you to gain practical advice based on their experience and hindsight.

Learning from others' mistakes not only saves you time and money, but also enhances the likelihood of your venture becoming a financial success.

Undertake work experience with a successful oyster farm

Gaining hands-on experience in an oyster farm provides insights into the day-to-day operations, and challenges specific to the activity.

This firsthand knowledge is crucial for effective planning and management if you decide to start your own oyster farm.

You'll also realise if the working hours suit your lifestyle. For many entrepreneurs, this can be a "make or break" situation, especially if they have children to look after.

First-hand experience will not only ensure that this is the right business opportunity for you, but will also enable you to meet valuable contacts and gain a better understanding of customer expectations and key success factors which will likely prove advantageous when launching your own oyster farm.

Participate in a training course

Undertaking training within your chosen industry is another way to get a feel for how an oyster farm works before deciding to pursue a new venture.

Whichever approach you go for to gain insights before starting your oyster farm, make sure you familiarise yourself with:

- The expertise needed to run the business successfully (do you have the skills required?)

- How a week of running an oyster farm might look like (does this fit with your personal situation?)

- The potential turnover of your oyster farm and long-term growth prospects (does this match your ambition?)

- The likely course of action if you decide to sell the company or retire (it's never too early to consider your exit)

At the end of this stage, you should be able to decide whether opening an oyster farm is the right business idea for you given your current personal situation (skills, desires, money, family, etc.).

Can your business idea be profitable?

Just enter your data and let The Business Plan Shop crunch the numbers. We will tell if your business idea can generate profits and cash flows, and how much you need to get started.

Assemble your oyster farm's founding team

The next step to start your oyster farm is to think about the ideal founding team, or to go in alone (which is always an option).

Setting up a business with several partners is a way of reducing the (high) risk of launching an oyster farm since it allows the financial risk of the project to be shared between the co-founders.

This also allows the company to benefit from a greater diversity of profiles in the management team and to spread the burden of decision-making over several shoulders.

But, running a business with multiple co-founders brings its own challenges. Disagreements between co-founders are quite common, and these can pose risks to the business. That's why it's crucial to consider all aspects before starting your business.

To make an informed decision, we suggest asking yourself these questions:

- How many co-founders would increase the project's chances of success?

- Do you and your potential partners share the same aspirations for the project?

- What is your plan B in case of failure?

Let's examine each of these questions in detail.

How many co-founders would increase the project's chances of success?

The answer to this question will depend on a number of factors, including:

- Your savings compared with the amount of initial capital needed to launch the oyster farm

- The skills you have compared with those needed to make a success of such a project

- How you want key decisions to be taken in the business (an odd number of partners or a majority partner is generally recommended to avoid deadlock)

Put simply, your partners contribute money and/or skills, and increasing the number of partners is often a good idea when one of these resources is in short supply.

Do you and your potential partners share the same aspirations for the project?

One of the key questions when selecting your potential partners will be their expectations. Do you want to create a small or large business? What are your ambitions for the next 10 or 15 years?

It's better to agree from the outset on what you want to create to avoid disagreements, and to check that you stay on the same wavelength as the project progresses to avoid frustration.

What is your plan B in case of failure?

Of course, we wish you every success, but it's wise to have a plan B when setting up a business.

How you handle the possibility of things not working out can depend a lot on the kind of relationship you have with your co-founders (like being a close friend, spouse, former colleague, etc.) and each person's individual situation.

Take, for instance, launching a business with your spouse. It may seem like a great plan, but if the business doesn't succeed, you could find yourself losing the entire household income at once, and that could be quite a nerve-wracking situation.

Similarly, starting a business partnership with a friend has its challenges. If the business doesn't work out or if tough decisions need to be made, it could strain the friendship.

It's essential to carefully evaluate your options before starting up to ensure you're well-prepared for any potential outcomes.

Is there room for another oyster farm on the market?

The next step in starting an oyster farm is to undertake market research. Now, let's delve into what this entails.

The objectives of market research

The goal here is straightforward: evaluate the demand for your business and determine if there's an opportunity to be seized.

One of the key points of your market analysis will be to ensure that the market is not saturated by competing offers.

The market research to open your oyster farm will also help you to define a concept and market positioning likely to appeal to your target clientele.

Finally, your analysis will provide you with the data you need to assess the revenue potential of your future business.

Let's take a look at how to carry out your market research.

Evaluating key trends in the sector

Market research for an oyster farm usually begins with an analysis of the sector in order to develop a solid understanding of its key players, and recent trends.

Assessing the demand

After the sector analysis comes demand analysis. Demand for an oyster farm refers to customers likely to consume the products and services offered by your company or its competitors.

Looking at the demand will enable you to gain insights into the desires and needs expressed by your future customers and their observed purchasing habits.

To be relevant, your demand analysis must be targeted to the geographic area(s) served by your company.

Your demand analysis should highlight the following points:

- Who buys the type of products and services you sell?

- How many potential customers are there in the geographical area(s) targeted by your company?

- What are their needs and expectations?

- What are their purchasing habits?

- How much do they spend on average?

- What are the main customer segments and their characteristics?

- How to communicate and promote the company's offer to reach each segment?

Analyzing demand helps pinpoint customer segments your oyster farm could target and determines the products or services that will meet their expectations.

Assessing the supply

Once you have a clear vision of who your potential customers are and what they want, the next step is to look at your competitors.

Amongst other things, you’ll need to ask yourself:

- What brands are competing directly/indirectly against your oyster farm?

- How many competitors are there in the market?

- Where are they located in relation to your company's location?

- What will be the balance of power between you and your competitors?

- What types of services and products do they offer? At what price?

- Are they targeting the same customers as you?

- How do they promote themselves?

- Which concepts seem to appeal most to customers?

- Which competitors seem to be doing best?

The aim of your competitive analysis will be to identify who is likely to overshadow you, and to find a way to differentiate yourself (more on this see below).

Regulations

Market research is also an opportunity to look at the regulations and conditions required to do business.

Ask yourself the following questions:

- Do you need a special degree to open an oyster farm?

- Are there necessary licences or permits?

- What are the main laws applicable to your future business?

At this stage, your analysis of the regulations should be carried out at a high level, to familiarize yourself with any rules and procedures, and above all to ensure that you meet the necessary conditions for carrying out the activity before going any further.

You will have the opportunity to come back to the regulation afterwards with your lawyer when your project is at a more advanced stage.

Take stock of the lessons learned from your market analysis

Market research should give you a definitive idea of your business idea's chances of commercial success.

Ideally, the conclusion is that there is a market opportunity because one or more customer segments are currently underserved by the competition.

On the other hand, the conclusion may be that the market is already taken. In this case, don't panic: the first piece of good news is that you're not going to spend several years working hard on a project that has no chance of succeeding. The second is that there's no shortage of ideas out there: at The Business Plan Shop, we've identified over 1,300 business start-up ideas, so you're bound to find something that will work.

Need a convincing business plan?

The Business Plan Shop makes it easy to create a financial forecast and write a business plan to help convince investors that your business idea can be profitable.

Choosing the right concept and positioning for your oyster farm

Once your market research is completed, it's time to consider the type of oyster farm you want to open and define precisely your company's market positioning in order to capitalise on the opportunity you identified during your market research.

Market positioning refers to the place your product and service offering occupies in customers' minds and how they differ from competing products and services. Being perceived as the premium solution, for example.

There are four questions you need to consider:

- How will you compete with and differentiate yourself from competitors already on the market?

- Is it better to start or buy an oyster farm already in operation?

- How will you validate your concept and market positioning?

Let's look at each of these in a little more detail.

How will you compete with and differentiate yourself from competitors already on the market?

When you choose to start up an oyster farm, you are at a disadvantage compared to your rivals who have an established presence on the market.

Your competitors have a reputation, a loyal customer base and a solid team already in place, whereas you're starting from scratch...

Entering the market and taking market share from your competitors won't happen automatically, so it's important to carefully consider how you plan to establish your presence.

There are four questions to consider here:

- Can you avoid direct competition by targeting a customer segment that is currently poorly served by other players in the market?

- Can you offer something unique or complementary to what is already available on the market?

- How will you build a sustainable competitive advantage for your oyster farm?

- Do you have the resources to compete with well-established competitors on your own, or would it be wiser to explore alternative options?

Also, think about how your competitors will react to your arrival on their market.

Is it better to start or buy an oyster farm already in operation?

An alternative to opening a new business is to take over an oyster farm already trading.

Purchasing an existing oyster farm means you get a loyal customer base and an efficient team. It also avoids disrupting the equilibrium in the market by introducing a new player.

A takeover hugely reduces the risk of the business failing compared to starting a new business, whilst giving you the freedom to change the market positioning of the business taken over if you wish.

This makes buying an existing oyster farm a solid alternative to opening your own.

However, buying a business requires more capital compared to starting an oyster farm from scratch, as you will need to purchase the business from its current owner.

How will you validate your concept and market positioning?

Regardless of how you choose to establish your business, it's crucial to make sure that the way you position your company aligns with the expectations of your target market.

To achieve this, you'll have to meet with your potential customers to showcase your products or services and get their feedback.

Explore the ideal location to start your oyster farm

The next stage in our guide on how to start an oyster farm: choosing where to set up shop.

Setting up your business in the right location will have a direct impact on your chances of success, so it's a good idea to think things through before you launch.

To help you decide where to set up your business, we recommend considering the following factors:

- Proximity to target customers - This is important for an oyster farm because it ensures a steady flow of customers and potential customers who are interested in purchasing fresh oysters.

- Climate and soil quality - Oysters are highly sensitive to environmental conditions, so it is crucial to have a location with the right climate and soil quality for optimal growth and taste.

- Availability of skilled labor - Oyster farming requires skilled labor for tasks such as shucking, grading, and harvesting. A location with a pool of experienced workers can ensure efficient operation of the farm.

- Premises layout - The layout of the premises should be suitable for oyster farming, with access to water and proper drainage to maintain the water quality.

These criteria will need to be refined according to the specific features of your project.

After weighing the factors mentioned earlier, it's crucial to focus on your startup's budget. Look for a location that suits your business needs while being affordable, especially in the short term.

One of the issues that will also come up is the long-term future of your location, particularly if you opt to rent your premises rather than buy. In this case, you will need to consider the conditions for renewing the lease (duration, rent increases, etc.).

Lease agreements vary widely from country to country, so make sure you check the terms applicable to your situation and have your lawyer review your lease before you sign.

Need inspiration for your business plan?

Avoid writer's block and draft your own business plan in no time by drawing inspiration from dozens of business plan templates.

What legal form should I choose for my oyster farm?

The next step to start an oyster farm is to choose the legal form of your business.

The legal form of a business simply means the legal structure it operates under. This structure outlines how the business is set up and defines its legal obligations and responsibilities.

Choosing the right legal form for your oyster farm is important because this will affect:

- Taxation: your tax obligations depend on the legal structure you choose, and this principle applies to both personal income tax and business taxes.

- Risk exposure: some legal structures have a legal personality (also known as corporate personality) and limited liability, which separates them from the owners running the business. This means that the business would be liable rather than the owners if things were to go wrong (lawsuit, debt owed in case of bankruptcy, etc.).

- Decision-making and governance: how you make key decisions varies based on the legal form of your business. In some cases you might need to have a board of directors and organise general assemblies to enable shareholders to influence major decisions with their voting rights.

- Financing: securing funding from investors requires you to have a company and they will expect limited liability and corporate personality to protect them legally.

- Paperwork and legal formalities: the legal structure you select determines whether certain obligations are necessary, such as producing annual accounts, or getting your books audited.

Deciding on a legal form is easy once you've estimated your sales, decided whether or not you need employees and figured out the number of co-founders joining you.

It's also essential to remember that a solid business idea will succeed no matter which legal structure you pick. Tax laws change regularly, so you can't rely on specific tax advantages tied to a particular structure when starting a business.

A proven approach is to look at what legal structures your top competitors are using, and go with the most common option as a working assumption. Once your idea is mature enough, and you're getting closer to officially registering your business, you can get advice from a lawyer and an accountant to confirm your choice.

Can your business idea be profitable?

Just enter your data and let The Business Plan Shop crunch the numbers. We will tell if your business idea can generate profits and cash flows, and how much you need to get started.

Assess the startup costs for an oyster farm

The next step in creating an oyster farm involves thinking about the equipment and staff needed for the business to operate.

After figuring out what you need for your business, your financial plan will reveal how much money you'll need to start and how much you might make (check below for more details).

Because every venture is distinctive, providing a reliable one-size-fits-all budget for launching an oyster farm without knowing the specifics of your project is not feasible.

Each project has its own particularities (size, concept, location), and only a forecast can show the exact amount required for the initial investment.

The first thing you'll need to consider is the equipment and investments you'll need to get your business up and running.

Startup costs and investments to launch your oyster farm

For an oyster farm, the initial working capital requirements (WCR) and investments could include the following elements:

- Oyster Cages: These are structures used to hold and grow oysters in the water. They are typically made of metal or plastic and can be expensive to purchase and maintain. You will need to budget for the initial purchase, as well as any repairs or replacements that may be needed.

- Boats and Equipment: Depending on the size of your oyster farm, you may need to invest in boats and equipment such as dredges, rakes, and hauling equipment. These are essential for harvesting and maintaining your oyster beds, and can be a significant capital expenditure.

- Water Quality Monitoring Equipment: Oysters are highly sensitive to changes in water quality, so it is important to have equipment to monitor and maintain the quality of the water in your farm. This can include items such as water testing kits, pH meters, and dissolved oxygen meters.

- Processing and Packaging Equipment: If you plan to sell your oysters, you will need to invest in equipment for processing and packaging them. This can include shucking machines, sorting tables, and packaging materials. These items can be costly, but they are essential for ensuring the quality and safety of your product.

- Land and Lease Costs: While not a physical asset, the cost of leasing or purchasing land for your oyster farm is a significant capital expenditure. You will need to consider the location, size, and accessibility of the land, as well as any ongoing lease or property taxes that may be required.

Of course, you will need to adapt this list to your business specificities.

Staffing plan of an oyster farm

In addition to equipment, you'll also need to consider the human resources required to run the oyster farm on a day-to-day basis.

The number of recruitments you need to plan will depend mainly on the size of your company.

Once again, this list is only indicative and will need to be adjusted according to the specifics of your oyster farm.

Other operating expenses for an oyster farm

While you're thinking about the resources you'll need, it's also a good time to start listing the operating costs you'll need to anticipate for your business.

The main operating costs for an oyster farm may include:

- Staff costs: This includes the salaries and benefits of your oyster farm employees, such as farm workers, harvesters, and administrative staff.

- Accountancy fees: You will need to hire an accountant to help you with bookkeeping, tax preparation, and financial reporting for your oyster farm.

- Insurance costs: It is important to have insurance coverage for your oyster farm to protect against potential risks such as property damage, liability claims, and crop loss.

- Software licenses: You may need to purchase software licenses for programs that help with record-keeping, inventory management, and sales tracking for your oyster farm.

- Banking fees: You will incur fees for banking services such as depositing checks, wire transfers, and credit card processing for your oyster farm's sales.

- Seed and spat costs: These are the costs associated with purchasing baby oysters (seed) or young oysters (spat) to grow on your oyster farm.

- Equipment and supplies: You will need to purchase and maintain equipment and supplies for your oyster farm, such as boats, cages, nets, and tools.

- Utilities: You will need to pay for utilities such as electricity, water, and fuel to operate your oyster farm.

- Marketing expenses: It is important to promote your oyster farm to attract customers. This may include costs for advertising, website development, and promotional materials.

- Transportation costs: You will need to transport your oysters from the farm to market or processing facilities, which may incur costs for fuel, vehicle maintenance, and shipping fees.

- Permit and licensing fees: You will need to obtain permits and licenses to operate your oyster farm, and these may have associated fees.

- Maintenance and repairs: Regular maintenance and repairs are necessary to keep your oyster farm in good condition, which may include costs for labor, materials, and equipment.

- Harvesting and processing costs: You may need to hire workers or purchase equipment to harvest and process your oysters for sale.

- Taxes: Your oyster farm may be subject to various taxes, including income tax, property tax, and sales tax.

- Education and training: It is important to stay up-to-date with oyster farming practices and regulations, so you may need to budget for education and training opportunities.

Like for the other examples included in this guide, this list will need to be tailored to your business but should be a good starting point for your budget.

Create a sales & marketing plan for your oyster farm

The next step to launching your oyster farm is to think about the actions you need to take to promote your products and services and build customer loyalty.

Here, you'll be looking at the following issues:

- What is the best method to attract as many new customers as possible?

- How to build customer loyalty and spread word of mouth?

- What human and financial resources will be required to implement the planned actions?

- What level of sales can I expect to generate in return?

The precise sales and marketing levers to activate will depend on the size of your oyster farm. But you could potentially leverage some of the initiatives below.

Besides your sales and marketing plan, your sales forecast will be affected by seasonal patterns related to the nature of your business, such as fluctuations during the holiday season, and your competitive landscape.

Can your business idea be profitable?

Just enter your data and let The Business Plan Shop crunch the numbers. We will tell if your business idea can generate profits and cash flows, and how much you need to get started.

Build your oyster farm's financial forecast

The next step to start your oyster farm: putting your financial projections together.

What is the financial forecast for an oyster farm?

A forecast is a quantified decision-making document that shows the initial investment required to open an oyster farm and the company's potential profitability and cash flow generation over the next 3 to 5 years.

As you think about your oyster farm idea, the main role of financial projections will be to help you decide whether it makes sense to create the company.

Building a financial forecast helps determine the amount of initial financing required to start your oyster farm.

In fact, creating financial projections is the only way to assess the amount of initial financing you'll need to open your oyster farm, and to make sure your project makes economic and financial sense.

Keep in mind that very few business ideas are financially viable. At The Business Plan Shop, we've seen nearly a million business start-up ideas, and we estimate that less than one in four is economically viable.

Your forecast will therefore require your full attention and constant revision, as your project matures. It's also a good idea to simulate different scenarios to anticipate several possibilities (what happens if your sales take longer than expected to ramp up, for example), so you're ready for all eventualities.

When seeking financing, your forecast will be incorporated into your business plan, which is the document you will use to present your business idea to financial partners. We'll come back to the business plan in more detail later in this guide.

Creating and updating your oyster farm's forecast is an ongoing process. Indeed, having up-to-date financial projections is the only way to maintain visibility over your company's future cash flow and cash position.

Forecasting is, therefore, the financial management tool that will be with you throughout the life of your company. Once you've started trading, you'll need to regularly compare the difference between your actual accounts and your forecasts, and then adjust them to maintain visibility over your future cash flows.

What does a financial forecast look like?

Once ready, your oyster farm forecast will be presented using the financial tables below.

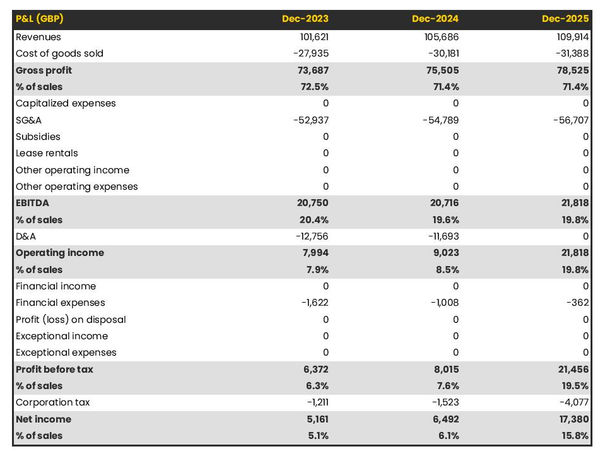

The forecasted profit & loss statement

The profit & loss forecast gives you a clear picture of your business’ expected growth over the first three to five years, and whether it’s likely to be profitable or not.

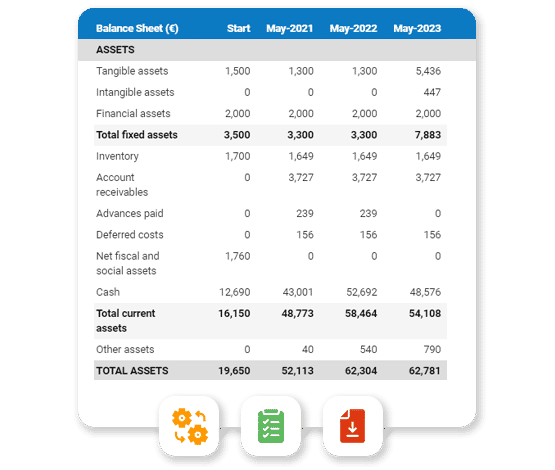

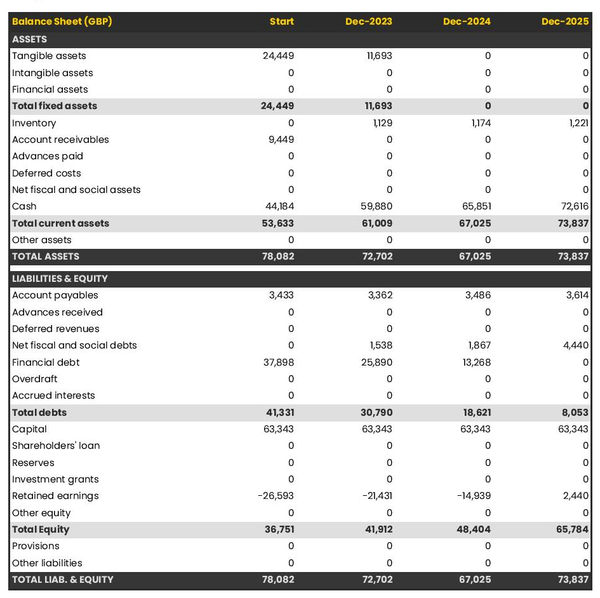

The projected balance sheet

Your oyster farm's forecasted balance sheet enables you to assess your financial structure and working capital requirements.

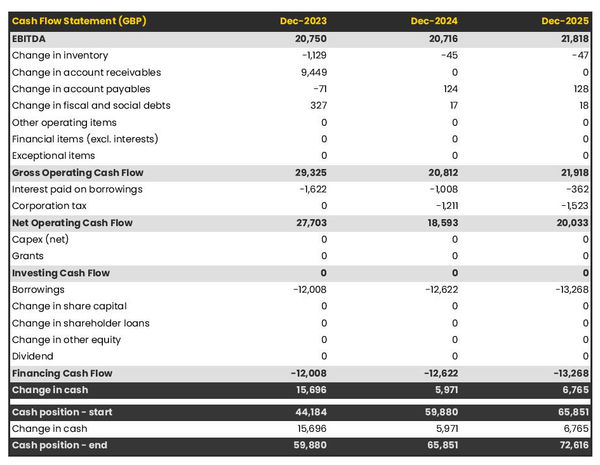

The projected cash flow statement

A projected cash flow statement to start an oyster farm is used to show how much cash the business is expected to generate or consume over the first three years.

Which solution should you use to make a financial projection for your oyster farm?

Using an online financial forecasting tool, such as the one we offer at The Business Plan Shop, is the simplest and safest solution for forecasting your oyster farm.

There are several advantages to using specialised software:

- You can easily create your financial forecast by letting the software take care of the financial calculations for you without errors

- You have access to complete financial forecast templates

- You get a complete financial forecast ready to be sent to your bank or investors

- The software helps you identify and correct any inconsistencies in your figures

- You can create scenarios to stress-test your forecast's main assumptions to stress-test the robustness of your business model

- After you start trading, you can easily track your actual financial performance against your financial forecast, and recalibrate your forecast to maintain visibility on your future cash flows

- You have a friendly support team on standby to assist you when you are stuck

If you are interested in this type of solution, you can try our forecasting software for free by signing up here.

Choose a name and register your oyster farm

The next phase in launching your oyster farm involves selecting a name for your company.

This stage is trickier than it seems. Finding the name itself is quite fun; the difficulty lies in finding one that is available and being the first to reserve it.

You cannot take a name that is similar to a name already used by a competitor or protected by a registered trademark without inevitably risking legal action.

So you need to find a name that is available, and be able to register it before someone else can.

In addition, you will probably want to use the same name for:

- Your company’s legal name - Example LTD

- Your business trading name - Example

- The trademark - Example ®

- Your company’s domain name - Example.com

The problem is that the procedures for registering these different names are carried out in different places, each with their own deadlines:

- Registering a domain name takes only a few minutes

- Registering a new trademark takes at least 12 weeks (if your application is accepted)

- The time taken to register a new business depends on the country, but it's generally fast

You will therefore be faced with the choice of: either registering everything at once and hoping that your name will be accepted everywhere, or proceeding step by step in order to minimise costs, but taking the risk that someone else will register one of the names you wanted in the meantime.

Our advice is to discuss strategy with your legal counsel (see further down in this guide) and prioritise your domain names and registered trademarks. You'll always have the option of using a trade name that's different from your company's legal name, and that's not a big deal.

To check that the name you want is not already in use, you should consult:

- Your country's business register

- The relevant trademark registers depending on which countries you want to register your trade mark in

- A domain name reservation company such as GoDaddy

- An Internet search engine

In this area too, your legal counsel will be able to help with the research and formalities.

Need inspiration for your business plan?

Avoid writer's block and draft your own business plan in no time by drawing inspiration from dozens of business plan templates.

Develop your oyster farm's corporate identity

The next step to launching an oyster farm: defining your company's visual identity.

Your corporate identity defines how your company's values are communicated visually. It makes you unique and allows you to stand out visually from your competitors and be recognized by your customers.

Defining your corporate identity can easily be done by you and your co-founders, using the many free tools available to generate color palettes, logos and other graphic elements. Nevertheless, this task is often best entrusted to a designer or agency to achieve a professional result.

Your oyster farm's visual identity will include the following elements:

- Logo

- Brand guidelines

- Business cards

- Website theme

Logo

The goal is to have stakeholders identify your business logo quickly and relate to it. Your logo will be used for media purposes (website, social networks, business cards, etc.) and legal documents (invoices, contracts, etc.).

The design of your logo must be emblematic, but it's also important that it can be seen on any type of support. To achieve this, it should be easily available in a range of colors, so that it stands out on both light and dark backgrounds.

Brand guidelines

The brand guidelines of your oyster farm act as a safeguard to ensure that your image is consistent whatever the medium used.

Brand guidelines lay out the details like the typography and colors to use to represent your company.

Typography refers to the fonts used (family and size). For example, Arial in size 26 for your titles and Tahoma in size 15 for your texts.

When it comes to the colors representing your brand, it's generally a good idea to stick to five or fewer:

- The main colour,

- A secondary colour (the accent),

- A dark background colour (blue or black),

- A grey background colour (to vary from white),

- Possibly another secondary colour.

Business cards

A rare paper medium that continues to survive digitalization, business cards are still a must-have for communicating your oyster farm contact details to your customers, suppliers and other partners.

In principle, they will include your logo and the brand guidelines we mentioned above.

Website theme

Likewise, the theme of your oyster farm website will include your logo and follow the brand guidelines we discussed earlier.

This will also define the look and feel of the main visual elements on your website:

- Buttons

- Menus

- Forms

- Banners

- Etc.

Understanding the legal and regulatory steps involved in opening an oyster farm

The next step in opening an oyster farm is to take the necessary legal and regulatory steps.

We recommend that you be accompanied by a law firm for all of the steps outlined below.

Registering a trademark and protecting the intellectual property of your oyster farm

The first step is to protect your company's intellectual property.

As mentioned earlier in this guide, you have the option to register a trademark. Your lawyer can assist you with a thorough search to ensure your chosen trademark is unique and doesn't conflict with existing ones and help select the classes (economic activities) and jurisdictions in which to register your trademark.

Your lawyer will also be able to advise you on other steps you could take to protect your company's other intellectual property assets.

Drafting the contractual documents for your oyster farm

Your oyster farm will rely on a set of contracts and legal documents for day-to-day operations.

Once again, we strongly recommend that you have these documents drawn up by a lawyer.

Your exact needs will depend on the country in which you are launching your oyster farm and the size of the company you are planning.

However, you may wish to consider the following documents at a minimum:

- Employment contracts

- General terms and conditions of sale

- General terms and conditions of use for your website

- Privacy Policy for your website

- Cookie Policy for your website

- Invoices

- Etc.

Applying for licences and permits and registering for various taxes

The licenses and permits needed for your business will depend on the country where you are establishing it. Your lawyer can guide you on the regulations relevant to your activity.

Similarly, your chartered accountant will be able to help you register for taxes and take the necessary steps to comply with the tax authorities.

Need a convincing business plan?

The Business Plan Shop makes it easy to create a financial forecast and write a business plan to help convince investors that your business idea can be profitable.

Create a business plan for your oyster farm

The next step to open an oyster farm: put together your business plan.

What is a business plan?

To keep it simple, a business plan comprises two crucial components:

- Firstly, a numerical part, the financial forecast (which we mentioned earlier), which highlights the initial financing requirements and profitability potential of the oyster farm,

- And a written, well-argued section that presents your project in detail, aims to convince the reader of its chances of success, and provides the context needed to assess whether the forecast is realistic or not.

The business plan will enable you to verify the coherence of your project, and ensure that the company can be profitable before incurring further costs. It will also help you convince business and financial partners.

As you can see, your business plan must be convincing and error-free.

How to write a business plan for an oyster farm?

Nowadays, the modern and most efficient way to write an oyster farm business plan is to use startup business plan software like the one we offer at The Business Plan Shop.

Using The Business Plan Shop to create a business plan for anoyster farm has several advantages :

- You can easily create your financial forecast by letting the software take care of the financial calculations for you without errors

- You are guided through the writing process by detailed instructions and examples for each part of the plan

- You can access a library of dozens of complete startup business plan samples and templates for inspiration

- You get a professional business plan, formatted and ready to be sent to your bank or investors

- You can create scenarios to stress test your forecast's main assumptions

- You can easily track your actual financial performance against your financial forecast by importing accounting data

- You can easily update your forecast as time goes by to maintain visibility on future cash flows

- You have a friendly support team on standby to assist you when you are stuck

If you're interested in using this type of solution, you can try The Business Plan Shop for free by signing up here.

Need a convincing business plan?

The Business Plan Shop makes it easy to create a financial forecast and write a business plan to help convince investors that your business idea can be profitable.

How to raise finance for my oyster farm?

Once your business plan has been drafted, you’ll need to think about how you might secure the financing necessary to open your oyster farm.

The amount of initial financing required will obviously depend on the size of your oyster farm and the country in which you wish to set up.

Businesses have access to two main categories of financing: equity and debt. Let's take a closer look at how they work and what sources are available.

Equity funding

At a high level, the equity of your oyster farm will consist of the money that founders and potential investors will invest to launch the company.

Equity is indispensable as it provides the company with a source of long-term (often permanent) financing and demonstrates the founders' conviction in the company's chances of success, since their investments would be lost in the event of bankruptcy.

Equity investors can generate a return on their investment through dividends (which can only be paid out if the company is profitable) or capital gains on the resale of their shares (if the company is attractive enough to attract a buyer).

As you can see, the equity investors' position is extremely risky, since their capital is at risk and can be lost in the event of bankruptcy, and the company must be profitable or resellable before they can hope to generate a return on their investment.

On the other hand, the return on investment that equity investors can expect to generate by investing in an oyster farm can be very substantial if the company is successful.

This is why equity investors look for start-up ideas with very high growth or profitability potential, in order to offset their risk with a high potential return on investment.

In technical terms, equity includes:

- Share capital and premiums: which represent the amount invested by the shareholders. This capital is considered permanent as it is non-refundable. In return for their investment, shareholders receive shares that entitle them to information, decision-making power (voting in general assembly), and the potential to receive a portion of any dividends distributed by the company.

- Director loans: these are examples of non-permanent capital advanced to the company by the shareholders. This is a more flexible way of injecting some liquidity into your company than doing so as you can repay director loans at any time.

- Reserves: these represent the share of profits set aside to strengthen the company's equity. Allocating a percentage of your profits to the reserves can be mandatory in certain cases (legal or statutory requirement depending on the legal form of your company). Once allocated in reserves, these profits can no longer be distributed as dividends.

- Investment grants: these represent any non-refundable amounts received by the company to help it invest in long-term assets.

- Other equity: which includes the equity items which don't fit in the other categories. Mostly convertible or derivative instruments. For a small business, it is likely that you won't have any other equity items.

The main sources of equity are as follows:

- Money put into the business from the founders' personal savings.

- Money invested by private individuals, which can include business angels, friends, and family members.

- Funds raised through crowdfunding, which can take the form of either equity or donations (often in exchange for a reward).

- Government support to start-ups, for example, loans on favourable terms to help founders build up their start-up capital.

Debt funding

The other way to finance your oyster farm is to borrow. From a financial point of view, the risk/return profile of debt is the opposite of that of equity: lenders' return on investment is guaranteed, but limited.

When it borrows, your company makes a contractual commitment to pay the lenders by interest, and to repay the capital borrowed according to a pre-agreed schedule.

As you can see, the lenders' return on investment is independent of whether or not the company is profitable. In fact, the only risk taken by lenders is the risk of the company going bankrupt.

To avoid this risk, lenders are very cautious, only agreeing to finance when they are convinced that the borrowing company will be able to repay them without problems.

From the point of view of the company and its stakeholders (workforce, customers, suppliers, etc.), debt increases the risk of the venture, since the company is committed to repaying the capital whether or not it is profitable. So there's a certain distrust towards heavily indebted companies.

Companies borrow in two ways:

- Against their assets: this is the most common way of borrowing. The bank finances a percentage of the price of an asset (a vehicle or a building, for example) and takes the asset as collateral. If the company cannot repay, the bank seizes the asset and sells it to limit its losses.

- Against their future cash flows: the bank reviews the company's financial forecast to estimate how much the company can comfortably borrow and repay, and what terms (amount, interest rate, term, etc.) the bank is prepared to offer given the credit risk posed by the company.

When creating an oyster farm, the first option is often the only one available, as lenders are often reluctant to lend on the basis of future cash flows to a structure that has no track record.

The type of assets that can be financed using the first method is also limited. Lenders will want to be sure that they can dispose of foreclosed assets if needed, so they need to be assets that have an established second-hand market.

That being said, terms and conditions also depend on the lender: some banks are prepared to finance riskier projects, and not all have the same view of your company's credit risk. It also depends on the collateral you can offer to reduce risk, and on your relationship with the bank.

In terms of possible sources of borrowing, the main sources here are banks and credit institutions.

In some countries, it's also possible to borrow from private investors (directly or via crowdlending platforms) or other companies, but not everywhere.

Takeaways on how to finance an oyster farm

Multiple options are available to help you raise the initial financing you need to launch your oyster farm.

There are two types of financing available to companies. To open an oyster farm, an equity investment will be required and may be supplemented by bank financing.

Launching your oyster farm and monitoring progress against your forecast

Once you’ve secured financing, you will finally be ready to launch your oyster farm. Congratulations!

Celebrate the launch of your business and acknowledge the hard work that brought you here, but remember, this is where the real work begins.

As you know, 50% of business start-ups do not pass the five-year mark. Your priority will be to do everything to secure your business's future.

To do this, it is key to keep an eye on your business plan to ensure that you are on track to achieve your goals.

No one can predict the future with certainty, so it’s likely that your oyster farm's financial performance will differ from what you predicted in your forecast.

This is why it is recommended to make several forecasts:

- A base case (most likely)

- An optimistic scenario

- And a pessimistic scenario to test the robustness of your financial model

If you follow this approach, your numbers will hopefully be better than your optimistic case and you can consider accelerating your expansion plans. That’s what we wish you anyway!

If, unfortunately, your figures are below your base case (or worse than your pessimistic case), you will need to quickly put in place corrective actions, or consider stopping the activity.

The key, in terms of decision-making, is to regularly compare your real accounting data to your oyster farm's forecast to:

- Measure the discrepancies and promptly identify where the variances with your base case come from

- Adjust your financial forecast as the year progresses to maintain visibility on future cash flow and cash position

There is nothing worse than waiting for your accountant to prepare your year-end accounts, which can take several months after the end of your financial year (up to nine months in the UK for example), to realise that the performance over the past year was well below the your base case and that your oyster farm will not have enough cash to keep running over the next twelve months.

This is why using a financial forecasting solution that integrates with accounting software and offers actuals vs. forecast tracking out of the box, like the financial dashboards we offer at The Business Plan Shop, greatly facilitates the task and significantly reduces the risk associated with starting a business.

Need inspiration for your business plan?

Avoid writer's block and draft your own business plan in no time by drawing inspiration from dozens of business plan templates.

Key takeaways

- This guide outlines the 15 key steps to open an oyster farm.

- The financial forecast is the tool that will enable you to validate the financial viability of your business idea.

- The business plan is the document that will enable you to approach your financial and commercial partners to convince them of the strengths of your project and secure the financing you need to launch your business.

- The real work begins once you've launched your business, and the only way to maintain visibility of your company's future cash flow is to keep your forecast up to date.

- Using a financial planning and analysis platform that combines forecasting, business planning and actual vs. forecast tracking and monitoring, such as The Business Plan Shop, makes the process easier and reduces the risks involved in starting a business.

We hope this guide has helped you understand how to start an oyster farm. Please don't hesitate to contact us if you have any questions.

Also on The Business Plan Shop

Do you know someone who wants to know how to open an oyster farm? Share our guide with them!

Founder & CEO at The Business Plan Shop Ltd