How to open a debt collection agency?

Are you keen to open a debt collection agency but don't know where to begin? Then you're in luck because this guide will lead you through all the steps required to check if your business idea can be profitable and, if so, turn it into a reality.

Our guide is for prospective entrepreneurs who are thinking about starting a debt collection agency no matter how far they are in their journey - whether you’re just thinking about it or in the middle of market research this guide will be useful to you.

Think of this as your blueprint: we cover everything you need to know about opening a debt collection agency and what key decisions you’ll need to make along the way.

Ready? Let’s get started!

Understanding how a debt collection agency works

The very first step when exploring a business idea such as starting a debt collection agency is to make sure you understand how the business operates and makes money (which is what we call the business model).

This will not only give you an initial idea of how profitable the business can be, but it will also enable you to make sure that this is the right business idea for you, given your skills, start-up capital and family or personal lifestyle, in particular.

The best ways to get to grips with the debt collection agency's business model are to:

- Talk to debt collection agency owners with experience

- Work a few months in a debt collection agency already in operation

- Take a training course

Talk to debt collection agency owners with experience

Experienced debt collection agency owners have valuable insights and can provide practical advice based on their firsthand experiences.

They've likely encountered and overcome challenges that a newcomer might not anticipate. Learning from other’s mistakes can save you both time and money and potentially increase your venture’s chances of succeeding.

Work a few months in a debt collection agency already in operation

Obtaining work experience in the industry can be a crucial factor in confirming whether you truly want to start a debt collection agency, as it provides insight into the day-to-day activities.

For instance, if the working hours are longer than expected or if other business requirements don't align with your personal lifestyle or preferences, you might reconsider your entrepreneurial goals.

Even if you've decided that this business idea is a good fit for you, gaining work experience will still be valuable. It helps you better understand your target market and customer needs, which is likely to be beneficial when launching your own debt collection agency.

Take a training course

Obtaining training within your chosen industry is another way to get a feel for how a debt collection agency works before deciding to pursue a new venture.

Whatever approach you choose to familiarise yourself with the business, before going any further with your plans to open a debt collection agency, make sure you understand:

- What skills are required to run the business (compare this with your own skills)

- What a typical week in the business is like (compare this with your personal or family life)

- What is the potential turnover of a debt collection agency and the long-term growth prospects (compare this with your level of ambition)

- Your options once you decide to sell the business or retire (it's never too early to consider your exit)

Can your business idea be profitable?

Just enter your data and let The Business Plan Shop crunch the numbers. We will tell if your business idea can generate profits and cash flows, and how much you need to get started.

Assemble your debt collection agency's founding team

The next step to start your debt collection agency is to think about the ideal founding team, or to go in alone (which is always an option).

Setting up a business with several partners is a way of reducing the (high) risk of launching a debt collection agency since it allows the financial risk of the project to be shared between the co-founders.

This also allows the company to benefit from a greater diversity of profiles in the management team and to spread the burden of decision-making over several shoulders.

But, running a business with multiple co-founders brings its own challenges. Disagreements between co-founders are quite common, and these can pose risks to the business. That's why it's crucial to consider all aspects before starting your business.

To make an informed decision, we suggest asking yourself these questions:

- How many co-founders would increase the project's chances of success?

- Do you and your potential partners share the same aspirations for the project?

- What is your plan B in case of failure?

Let's examine each of these questions in detail.

How many co-founders would increase the project's chances of success?

The answer to this question will depend on a number of factors, including:

- Your savings compared with the amount of initial capital needed to launch the debt collection agency

- The skills you have compared with those needed to make a success of such a project

- How you want key decisions to be taken in the business (an odd number of partners or a majority partner is generally recommended to avoid deadlock)

Put simply, your partners contribute money and/or skills, and increasing the number of partners is often a good idea when one of these resources is in short supply.

Do you and your potential partners share the same aspirations for the project?

One of the key questions when selecting your potential partners will be their expectations. Do you want to create a small or large business? What are your ambitions for the next 10 or 15 years?

It's better to agree from the outset on what you want to create to avoid disagreements, and to check that you stay on the same wavelength as the project progresses to avoid frustration.

What is your plan B in case of failure?

Of course, we wish you every success, but it's wise to have a plan B when setting up a business.

How you handle the possibility of things not working out can depend a lot on the kind of relationship you have with your co-founders (like being a close friend, spouse, former colleague, etc.) and each person's individual situation.

Take, for instance, launching a business with your spouse. It may seem like a great plan, but if the business doesn't succeed, you could find yourself losing the entire household income at once, and that could be quite a nerve-wracking situation.

Similarly, starting a business partnership with a friend has its challenges. If the business doesn't work out or if tough decisions need to be made, it could strain the friendship.

It's essential to carefully evaluate your options before starting up to ensure you're well-prepared for any potential outcomes.

Is there room for another debt collection agency on the market?

The next step in starting a debt collection agency is to undertake market research. Now, let's delve into what this entails.

The objectives of market research

The goal here is straightforward: evaluate the demand for your business and determine if there's an opportunity to be seized.

One of the key points of your market analysis will be to ensure that the market is not saturated by competing offers.

The market research to open your debt collection agency will also help you to define a concept and market positioning likely to appeal to your target clientele.

Finally, your analysis will provide you with the data you need to assess the revenue potential of your future business.

Let's take a look at how to carry out your market research.

Evaluating key trends in the sector

Market research for a debt collection agency usually begins with an analysis of the sector in order to develop a solid understanding of its key players, and recent trends.

Assessing the demand

After the sector analysis comes demand analysis. Demand for a debt collection agency refers to customers likely to consume the products and services offered by your company or its competitors.

Looking at the demand will enable you to gain insights into the desires and needs expressed by your future customers and their observed purchasing habits.

To be relevant, your demand analysis must be targeted to the geographic area(s) served by your company.

Your demand analysis should highlight the following points:

- Who buys the type of products and services you sell?

- How many potential customers are there in the geographical area(s) targeted by your company?

- What are their needs and expectations?

- What are their purchasing habits?

- How much do they spend on average?

- What are the main customer segments and their characteristics?

- How to communicate and promote the company's offer to reach each segment?

Analyzing demand helps pinpoint customer segments your debt collection agency could target and determines the products or services that will meet their expectations.

Assessing the supply

Once you have a clear vision of who your potential customers are and what they want, the next step is to look at your competitors.

Amongst other things, you’ll need to ask yourself:

- What brands are competing directly/indirectly against your debt collection agency?

- How many competitors are there in the market?

- Where are they located in relation to your company's location?

- What will be the balance of power between you and your competitors?

- What types of services and products do they offer? At what price?

- Are they targeting the same customers as you?

- How do they promote themselves?

- Which concepts seem to appeal most to customers?

- Which competitors seem to be doing best?

The aim of your competitive analysis will be to identify who is likely to overshadow you, and to find a way to differentiate yourself (more on this see below).

Regulations

Market research is also an opportunity to look at the regulations and conditions required to do business.

Ask yourself the following questions:

- Do you need a special degree to open a debt collection agency?

- Are there necessary licences or permits?

- What are the main laws applicable to your future business?

At this stage, your analysis of the regulations should be carried out at a high level, to familiarize yourself with any rules and procedures, and above all to ensure that you meet the necessary conditions for carrying out the activity before going any further.

You will have the opportunity to come back to the regulation afterwards with your lawyer when your project is at a more advanced stage.

Take stock of the lessons learned from your market analysis

Market research should give you a definitive idea of your business idea's chances of commercial success.

Ideally, the conclusion is that there is a market opportunity because one or more customer segments are currently underserved by the competition.

On the other hand, the conclusion may be that the market is already taken. In this case, don't panic: the first piece of good news is that you're not going to spend several years working hard on a project that has no chance of succeeding. The second is that there's no shortage of ideas out there: at The Business Plan Shop, we've identified over 1,300 business start-up ideas, so you're bound to find something that will work.

Need a convincing business plan?

The Business Plan Shop makes it easy to create a financial forecast and write a business plan to help convince investors that your business idea can be profitable.

Choosing the right concept and positioning for your debt collection agency

Once your market research is completed, it's time to consider the type of debt collection agency you want to open and define precisely your company's market positioning in order to capitalise on the opportunity you identified during your market research.

Market positioning refers to the place your product and service offering occupies in customers' minds and how they differ from competing products and services. Being perceived as the premium solution, for example.

There are four questions you need to consider:

- How will you compete with and differentiate yourself from competitors already on the market?

- Is it better to start or buy a debt collection agency already in operation?

- How will you validate your concept and market positioning?

Let's look at each of these in a little more detail.

How will you compete with and differentiate yourself from competitors already on the market?

When you choose to start up a debt collection agency, you are at a disadvantage compared to your rivals who have an established presence on the market.

Your competitors have a reputation, a loyal customer base and a solid team already in place, whereas you're starting from scratch...

Entering the market and taking market share from your competitors won't happen automatically, so it's important to carefully consider how you plan to establish your presence.

There are four questions to consider here:

- Can you avoid direct competition by targeting a customer segment that is currently poorly served by other players in the market?

- Can you offer something unique or complementary to what is already available on the market?

- How will you build a sustainable competitive advantage for your debt collection agency?

- Do you have the resources to compete with well-established competitors on your own, or would it be wiser to explore alternative options?

Also, think about how your competitors will react to your arrival in their market.

Is it better to start or buy a debt collection agency already in operation?

An alternative to opening a new business is to take over a debt collection agency already trading.

Purchasing an existing debt collection agency means you get a loyal customer base and an efficient team. It also avoids disrupting the equilibrium in the market by introducing a new player.

A takeover hugely reduces the risk of the business failing compared to starting a new business, whilst giving you the freedom to change the market positioning of the business taken over if you wish.

This makes buying an existing debt collection agency a solid alternative to opening your own.

However, buying a business requires more capital compared to starting a debt collection agency from scratch, as you will need to purchase the business from its current owner.

How will you validate your concept and market positioning?

Regardless of how you choose to establish your business, it's crucial to make sure that the way you position your company aligns with the expectations of your target market.

To achieve this, you'll have to meet with your potential customers to showcase your products or services and get their feedback.

Where should I base my debt collection agency?

The next step in our guide on starting a debt collection agency involves making a key choice about where you want your business to be located.

Picking the ideal location for your business is like selecting the perfect canvas for a painting. Without it, your business might not showcase its true colors.

We recommend that you take the following factors into account when making your decision:

This list is not comprehensive and will have to be adjusted based on the details of your project.

The parameters to be taken into account will also depend on whether you opt to rent premises or buy them. If you are a tenant, you will need to consider the conditions attached to the lease: duration, rent increase, renewal conditions, etc.

Lease agreements differ widely from country to country, so it's essential to review the terms that apply to your situation. Before putting pen to paper, consider having your lawyer look carefully at the lease.

Need inspiration for your business plan?

Avoid writer's block and draft your own business plan in no time by drawing inspiration from dozens of business plan templates.

Choosing your debt collection agency's legal form

The next step to open a debt collection agency is to choose the legal form of your business.

The legal form of a business simply means the legal structure it operates under. This structure outlines how the business is set up and defines its legal obligations and responsibilities.

Why is your debt collection agency's legal form important?

Choosing the legal form for your debt collection agency is an important decision because this will affect your tax obligations, your personal exposure to risk, how decisions are made within the business, the sources of financing available to you, and the amount of paperwork and legal formalities, amongst other things.

The way you set up your business legally will impact your taxes and social contributions, both at a personal level (how much your income is taxed) and at the business level (how much the business's profits are taxed).

Your personal exposure to risk as a business owner also varies based on the legal form of your business. Certain legal forms have a legal personality (also called corporate personality), which means that the business obtains a legal entity which is separate from the owners and the people running it. To put it simply, if something goes wrong with a customer or competitor, for example, with a corporate personality the business gets sued, whereas without it is the entrepreneur personally.

Similarly, some legal forms benefit from limited liability. With a limited liability the maximum you can lose if the business fails is what you invested. Your personal assets are not at risk. However, not all structures protect you in such a way, some structures may expose your personal assets (for example, your creditors might try to go after your house if the business incurs debts and then goes under without being able to repay what it owed).

How decisions are made within the business is also influenced by the legal form of your debt collection agency, and so is the amount of paperwork and legal formalities: do you need to hold general assemblies, to produce annual accounts, to get the accounts audited, etc.

The legal form also influences what sources of financing are available to you. Raising capital from investors requires having a company set up, and they will expect limited liability and corporate personality.

What are the most common legal structures?

It's important to note that the actual names of legal structures for businesses vary from country to country.

But they usually fall within two main types of structures:

- Individual businesses

- Companies

Individual businesses

Individual businesses, such as sole traders or sole proprietorships, are legal structures with basic administrative requirements.

They primarily serve self-employed individuals and freelancers rather than businesses with employees.

The main downside of being a sole trader is that there's usually no legal separation between the business and the person running it. Everything the person owns personally is tied up with the business, which can be risky.

This means that if there are problems or the business goes bankrupt, the entrepreneur's personal assets could be taken by creditors. So, there's a risk of personal liability in case of disputes or financial issues.

It is also not possible to raise equity from investors with these structures as there is no share capital.

Despite the downsides, being a sole proprietorship has some advantages. There is usually very little paperwork to get started, simpler tax calculations and accounting formalities.

Companies

Companies are all rounders which can be set up by one or more individuals, working on their own or with many employees.

They are recognized as a distinct entity with their own legal personality, and the liability is usually limited to the amount invested by the owners (co-founders and investors). This means that you cannot lose more than you have invested in the business.

This separation ensures that in legal disputes or bankruptcy, the company bears primary responsibility, protecting the personal assets of the founder(s) and potential investor(s).

How should I choose my debt collection agency's legal structure?

Deciding on the legal structure is usually quite straightforward once you know how many co-founders you'll have, whether you'll have employees, and the expected revenues for the business.

A good business idea will be viable whatever the legal form you choose. How businesses are taxed changes every year, therefore one cannot rely on specific tax benefits tied to a particular structure when deciding to go into business.

One easy way to proceed is to take note of the legal structures used by your top five competitors, and assume you're going with the most commonly chosen option. Once your idea is mature and you're prepared to formally register the business, you can validate this assumption with a lawyer and an accountant.

Can I switch my debt collection agency's legal structure if I get it wrong?

You can switch your legal setup later on, even if it involves selling the old one to a new entity in some cases. However, this comes with extra costs, so it's better to make the right choice from the beginning if you can.

Can your business idea be profitable?

Just enter your data and let The Business Plan Shop crunch the numbers. We will tell if your business idea can generate profits and cash flows, and how much you need to get started.

Assess the startup costs for a debt collection agency

The next step in creating a debt collection agency involves thinking about the equipment and staff needed for the business to operate.

After figuring out what you need for your business, your financial plan will reveal how much money you'll need to start and how much you might make (check below for more details).

Because every venture is distinctive, providing a reliable one-size-fits-all budget for launching a debt collection agency without knowing the specifics of your project is not feasible.

Each project has its own particularities (size, concept, location), and only a forecast can show the exact amount required for the initial investment.

The first thing you'll need to consider is the equipment and investments you'll need to get your business up and running.

Startup costs and investments to launch your debt collection agency

For a debt collection agency, the initial working capital requirements (WCR) and investments could include the following elements:

- Debt Collection Software: This is a crucial tool for a debt collection agency as it helps in tracking and managing accounts, generating reports, and automating some processes. It is important to invest in reliable and efficient software to ensure smooth operations and maximize productivity.

- Computers and Hardware: In today's digital age, computers and other hardware are essential for a debt collection agency. These include desktops, laptops, printers, scanners, and other necessary equipment. These tools help in managing and organizing data, communicating with clients, and carrying out day-to-day operations.

- Office Furniture and Supplies: A debt collection agency requires a professional and comfortable workspace for its employees. This may include desks, chairs, filing cabinets, and other furniture. Office supplies such as stationery, pens, and paper are also necessary for day-to-day operations.

- Security Systems: As a debt collection agency deals with sensitive and confidential information, it is crucial to invest in security systems to protect data and assets. This may include CCTV cameras, alarms, and other security measures to prevent any unauthorized access.

- Debt Collection Training and Education: While training and education may fall under operating expenses, it is still a significant capital expenditure for a debt collection agency. Investing in training and education for employees ensures that they have the necessary skills and knowledge to effectively carry out their duties, resulting in higher success rates and increased revenue.

Of course, you will need to adapt this list to your business specificities.

Staffing plan of a debt collection agency

In addition to equipment, you'll also need to consider the human resources required to run the debt collection agency on a day-to-day basis.

The number of recruitments you need to plan will depend mainly on the size of your company.

Once again, this list is only indicative and will need to be adjusted according to the specifics of your debt collection agency.

Other operating expenses for a debt collection agency

While you're thinking about the resources you'll need, it's also a good time to start listing the operating costs you'll need to anticipate for your business.

The main operating costs for a debt collection agency may include:

- Staff costs: This includes salaries, benefits, and any other expenses related to your employees. As a debt collection agency, you will need a team of collectors to handle the accounts, as well as administrative staff to manage the day-to-day operations.

- Accountancy fees: You will need to hire a qualified accountant to manage your financial records, prepare your taxes, and provide advice on financial planning and budgeting.

- Insurance costs: As a debt collection agency, you will need to protect your business against potential lawsuits and other risks. This may include professional liability insurance, general liability insurance, and workers' compensation insurance.

- Software licenses: In order to efficiently manage your accounts and track collections, you will need to invest in debt collection software. This may include licenses for debt collection management systems, credit reporting software, and other related tools.

- Banking fees: You will need to maintain a business bank account to manage your finances and process payments from clients. This may include fees for transactions, account maintenance, and other related services.

- Marketing and advertising: In order to attract clients and grow your business, you will need to invest in marketing and advertising efforts. This may include online ads, direct mail campaigns, and other promotional materials.

- Office rent and utilities: You will need a physical office space to operate your debt collection agency. This may include rent, utilities, and other related expenses.

- Legal fees: As a debt collection agency, you may encounter legal issues such as disputes with clients or debtors. You will need to budget for legal fees to protect your business interests.

- Training and development: To ensure the success of your team, you may need to invest in ongoing training and development programs. This may include seminars, workshops, and other educational opportunities.

- Office supplies: You will need basic office supplies such as pens, paper, and printer ink to run your business on a daily basis.

- Telephone and internet expenses: As a debt collection agency, you will need to communicate with clients, debtors, and other parties on a regular basis. This will require a reliable telephone and internet connection, which may come with associated expenses.

- Travel and transportation: Depending on the size and scope of your business, you may need to travel for meetings, conferences, or site visits. This will incur expenses for transportation, lodging, and meals.

- Professional memberships and certifications: To stay up-to-date with industry trends and best practices, you may need to join professional organizations and obtain certifications. These may come with membership or renewal fees.

- External services: Depending on the needs of your business, you may need to outsource certain tasks to external service providers. This may include debt collection agencies, IT support, or marketing agencies.

- Taxes: As a business, you will be responsible for paying various taxes, including income tax, sales tax, and payroll taxes. Make sure to budget for these expenses accordingly.

Like for the other examples included in this guide, this list will need to be tailored to your business but should be a good starting point for your budget.

How will I promote my debt collection agency's?

The next step to starting a debt collection agency is to think about strategies that will help you attract and retain clients.

Consider the following questions:

- How will you attract as many customers as possible?

- How will you build customer loyalty?

- Who will be responsible for advertising and promotion? What budget can be allocated to these activities?

- How many sales and how much revenue can that generate?

Once again, the resources required will depend on your ambitions and the size of your company. But you could potentially action the initiatives below.

Your debt collection agency's sales plan will also be affected by variations in consumer demand, like changes in activity during peak holiday seasons, and the dynamics within your competitive environment.

Can your business idea be profitable?

Just enter your data and let The Business Plan Shop crunch the numbers. We will tell if your business idea can generate profits and cash flows, and how much you need to get started.

How do I build my debt collection agency financial forecast?

Let's now look at the financial projections you will need to prepare in order to open a debt collection agency.

What is a debt collection agency's financial projection?

Your financial forecast will help you budget your project so that you can evaluate:

- Its expected sales and growth potential

- Its expected profitability, to ensure that the business will be viable

- Its cash generation and financing requirements

Making your financial forecast is the only way to determine the amount of initial financing required to create your debt collection agency.

There are lots of business ideas out there, but very few of them are viable, and making a financial forecast is the only way to ensure that your project makes economic and financial sense.

Creating a debt collection agency financial projection is an iterative process, as you'll need to refine your figures as your business idea matures.

You'll start with a first high-level version to decide whether or not to continue working on the project.

Then, as your project takes shape, your forecasts will become increasingly accurate. You'll also need to test different assumptions to ensure that your idea of starting a debt collection agency holds up even if your trading environment deteriorates (lower sales than expected, difficulties in recruiting, sudden cost increases or equipment failure problems, for example).

Your financial forecast will be part of your overall business plan, which we'll look at in more detail later. Your financial partners will use your business plan to decide if they want to finance you.

Once you've launched your business, you can compare your actual accounting figures with your forecasts, to analyze where the discrepancies come from, and then update your forecasts to maintain visibility over your future cash flows.

Financial forecasts are, therefore, a financial management tool that will be with you throughout the life of your company.

What does a financial projection look like?

Your debt collection agency forecast will be presented using the following financial tables.

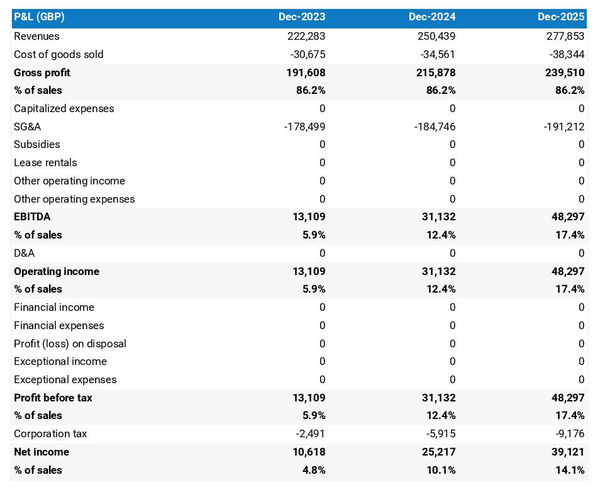

The projected P&L statement

The projected P&L statement for a debt collection agency shows how much revenue and profits your business is expected to generate in the future.

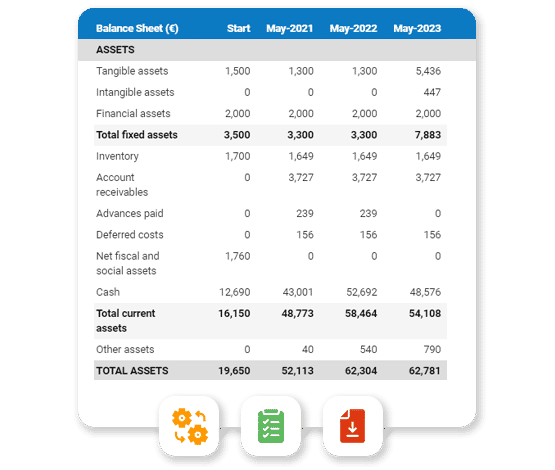

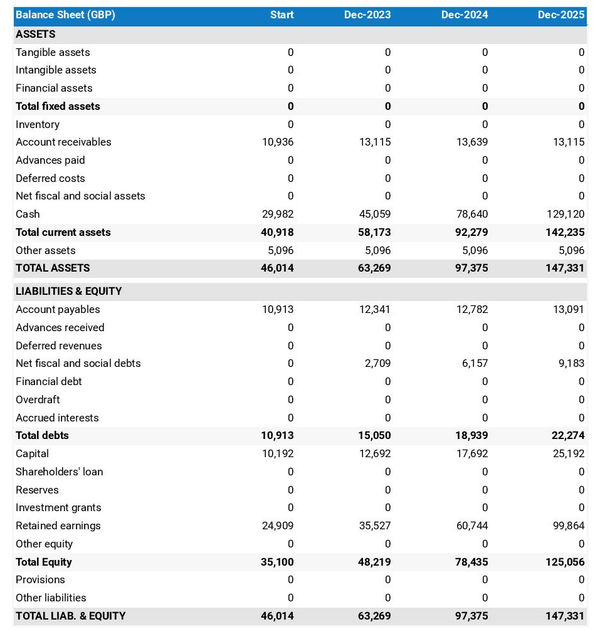

The projected balance sheet of your debt collection agency

Your debt collection agency's projected balance sheet provides a snapshot of your business’s financial position at year-end.

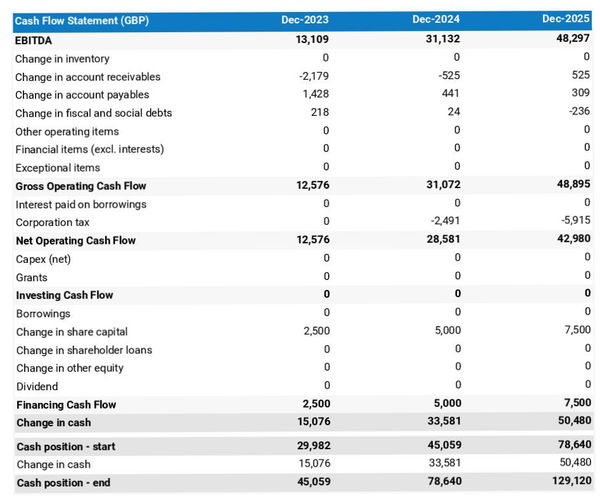

The cash flow forecast

A projected cash flow statement for a debt collection agency is used to show how much cash the business is expected to consume or generate in the years to come.

What is the best financial forecasting tool for starting your debt collection agency?

The simplest and easiest way to create your debt collection agency's projections is to use professional online financial forecasting software such as the one we offer at The Business Plan Shop.

There are several advantages to using specialised software:

- You can easily create your financial forecast by letting the software take care of the financial calculations for you without errors

- You have access to complete financial forecast templates

- You get a complete financial forecast ready to be sent to your bank or investors

- The software helps you identify and correct any inconsistencies in your figures

- You can create scenarios to stress-test your forecast's main assumptions to stress-test the robustness of your business model

- After you start trading, you can easily track your actual financial performance against your financial forecast, and recalibrate your forecast to maintain visibility on your future cash flows

- You have a friendly support team on standby to assist you when you are stuck

If you are interested in this type of solution, you can try our forecasting software for free by signing up here.

How do I choose a name and register my debt collection agency?

Now that your project of launching a debt collection agency is starting to take shape, it's time to look at the name of your business.

Finding the name itself is generally fairly easy. The difficulty lies in registering it.

To prevent this guide from being too long, we won't go into all the criteria you need to take into account when choosing a striking name for your debt collection agency. However, try to choose a name that is short and distinctive.

Once you have a name that you like, you need to check that it is available, because you cannot use a name that is identical or similar to that of a competitor: this type of parasitic behaviour is an act of unfair competition for which you risk being taken to court by your competitors.

To avoid any problems, you will need to check the availability of the name:

- Your country's company register

- With the trademark register

- With a domain name reservation company such as GoDaddy

- On an Internet search engine

If the desired name is available, you can start the registration process.

It is common to want to use the trading name as the name of the company, and to have a domain name and a registered trademark that also correspond to this name: Example ® (trading name protected by a registered trademark), Example LTD (legal name of the company), example.com (domain name used by the company).

The problem is that each of these names has to be registered with a different entity, and each entity has its own deadlines:

- Registering a domain name is immediate

- Registering a trademark usually takes at least 3 months (if your application is accepted)

- The time taken to register a new business depends on the country, but it's generally quite fast

How do I go about it?

Well, you have two choices:

- Complete all registrations at the same time and cross your fingers for a smooth process.

- Make sure to secure the domain names and trademarks. Once that's done, wait for confirmation of a successful trademark registration before moving on to register the company.

At The Business Plan Shop, we believe it's essential to prioritize securing your domain names and trademarks over the business name. This is because you have the flexibility to use a different trading name than your legal business name if needed.

Regardless, we suggest discussing this matter with your lawyer (see below in this guide) before making any decisions.

Need inspiration for your business plan?

Avoid writer's block and draft your own business plan in no time by drawing inspiration from dozens of business plan templates.

Develop your debt collection agency's corporate identity

The next step to launching a debt collection agency: defining your company's visual identity.

Your corporate identity defines how your company's values are communicated visually. It makes you unique and allows you to stand out visually from your competitors and be recognized by your customers.

Defining your corporate identity can easily be done by you and your co-founders, using the many free tools available to generate color palettes, logos and other graphic elements. Nevertheless, this task is often best entrusted to a designer or agency to achieve a professional result.

Your debt collection agency's visual identity will include the following elements:

- Logo

- Brand guidelines

- Business cards

- Website theme

Logo

The goal is to have stakeholders identify your business logo quickly and relate to it. Your logo will be used for media purposes (website, social networks, business cards, etc.) and legal documents (invoices, contracts, etc.).

The design of your logo must be emblematic, but it's also important that it can be seen on any type of support. To achieve this, it should be easily available in a range of colors, so that it stands out on both light and dark backgrounds.

Brand guidelines

The brand guidelines of your debt collection agency act as a safeguard to ensure that your image is consistent whatever the medium used.

Brand guidelines lay out the details like the typography and colors to use to represent your company.

Typography refers to the fonts used (family and size). For example, Arial in size 26 for your titles and Tahoma in size 15 for your texts.

When it comes to the colors representing your brand, it's generally a good idea to stick to five or fewer:

- The main colour,

- A secondary colour (the accent),

- A dark background colour (blue or black),

- A grey background colour (to vary from white),

- Possibly another secondary colour.

Business cards

A rare paper medium that continues to survive digitalization, business cards are still a must-have for communicating your debt collection agency contact details to your customers, suppliers and other partners.

In principle, they will include your logo and the brand guidelines we mentioned above.

Website theme

Likewise, the theme of your debt collection agency website will include your logo and follow the brand guidelines we discussed earlier.

This will also define the look and feel of the main visual elements on your website:

- Buttons

- Menus

- Forms

- Banners

- Etc.

Navigate the legal and regulatory requirements for launching your debt collection agency

The next thing to do in getting a debt collection agency off the ground is to handle all the legal and regulatory requirements. We recommend that you be accompanied by a law firm for all of the steps outlined below.

Intellectual property

One of your priorities will be to ensure that your company's intellectual property is adequately protected.

As explained before, you can choose to register a trademark. Your lawyer can help you with a detailed search to make sure your chosen trademark is unique and doesn't clash with existing ones.

They'll assist in preparing the required documents and steer you in picking the right categories and locations for trademark registration.

Moreover, your lawyer can offer guidance on additional measures to protect other intellectual property assets your company may have.

Getting your debt collection agency paperwork in order

For day-to-day operations, your debt collection agency will need to rely on a set of contractual documents.

Your exact needs in this respect will depend on the country in which you are launching your debt collection agency, the number of partners and the envisaged size of the company.

However, you will probably need at least the following documents:

- Employment contracts

- General terms and conditions of sale

- General terms and conditions of use for your website

- Privacy Policy for your website

- Cookie Policy for your website

- Invoices

- Etc.

Applying for licences and permits and registering for various taxes

Operating your business legally may require licences and business permits. The exact requirements applicable to your situation will depend on the country in which you set up your debt collection agency.

The lawyers who advise you will also be able to guide you with regard to all the rules applicable to your business.

Similarly, your accountant will be able to help you take the necessary steps to comply with the tax authorities.

Need a convincing business plan?

The Business Plan Shop makes it easy to create a financial forecast and write a business plan to help convince investors that your business idea can be profitable.

Writing a business plan for your debt collection agency

The next step in opening a debt collection agency is to draw up your business plan.

What is a debt collection agency's business plan?

A business plan serves as a comprehensive roadmap outlining the objectives, strategies, and key components of your venture.

There are two essential parts to a business plan:

- A numerical part, the financial forecast we mentioned earlier in this guide, which highlights the amount of initial financing needed to launch the business and its potential profitability over the next 3 to 5 years,

- A written part, which presents in detail the project of creating a debt collection agency and provides the necessary context to enable the reader of the business plan to judge the relevance and coherence of the figures included in the forecast.

Your business plan helps guide decision-making by showcasing your vision and financial potential in a coherent manner.

Your business plan will also be essential when you're looking for financing, as your financial partners will ask you for it when deciding whether or not to finance your project to open a debt collection agency. So it's best to produce a professional, reliable, and error-free business plan.

In essence, your business plan is the blueprint to turn your idea into a successful reality.

What tool should you use to create your debt collection agency business plan?

If you want to write a convincing business plan quickly and efficiently, a good solution is to use an online business plan software for business start-ups like the one we offer at The Business Plan Shop.

Using The Business Plan Shop to create a business plan for a debt collection agency has several advantages :

- You can easily create your financial forecast by letting the software take care of the financial calculations for you without errors

- You are guided through the writing process by detailed instructions and examples for each part of the plan

- You can access a library of dozens of complete startup business plan samples and templates for inspiration

- You get a professional business plan, formatted and ready to be sent to your bank or investors

- You can create scenarios to stress test your forecast's main assumptions

- You can easily track your actual financial performance against your financial forecast by importing accounting data

- You can easily update your forecast as time goes by to maintain visibility on future cash flows

- You have a friendly support team on standby to assist you when you are stuck

If you're interested in using our solution, you can try The Business Plan Shop for free by signing up here.

Need a convincing business plan?

The Business Plan Shop makes it easy to create a financial forecast and write a business plan to help convince investors that your business idea can be profitable.

Raise the financing needed to launch your debt collection agency

With your business plan in hand, you can tackle one of the final steps to open a debt collection agency business: the search for financing.

Raising the capital needed to launch your business will probably require a combination of equity and debt, which are the two types of financing available to companies.

Equity funding

Equity is the sum of money invested in a debt collection agency by both founders and investors.

Equity is a key factor in business start-ups. Should the project fail, the sums invested in equity are likely to be lost; these sums therefore enable the founders to send a strong signal to their commercial and financial partners as to their conviction in the project's chances of success.

In terms of return on investment, equity investors can either receive dividends from the company (provided it is profitable) or realize capital gains by selling their shares (provided a buyer is interested in the company).

Equity providers are therefore in a very risky position. They can lose everything in the event of bankruptcy, and will only see a return on their investment if the company is profitable or resold. On the other hand, they can generate a very high return if the project is a success.

Given their position, equity investors look for start-up projects with sufficient growth and profitability potential to offset their risk.

From a technical standpoint, equity includes:

- Share capital and premiums: which represent the amount invested by the shareholders. This capital is considered permanent as it is non-refundable. In return for their investment, shareholders receive shares that entitle them to information, decision-making power (voting in general assembly), and the potential to receive a portion of any dividends distributed by the company.

- Director loans: these are examples of non-permanent capital advanced to the company by the shareholders. This is a more flexible way of injecting some liquidity into your company as you can repay director loans at any time.

- Reserves: these represent the share of profits set aside to strengthen the company's equity. Allocating a percentage of your profits to the reserves can be mandatory in certain cases (legal or statutory requirement depending on the legal form of your company). Once allocated in reserves, these profits can no longer be distributed as dividends.

- Investment grants: which represent any non-refundable amounts received by the company to help it invest in long-term assets.

- Other equity: which includes the equity items which don't fit in the other categories. Mostly convertible or derivative instruments. For a small business, it is likely that you won't have any other equity items.

The main sources of equity are as follows:

- Contributions made by the owners.

- Private investors: business angels, friends and family.

- Crowdfunding: raising funds by involving a group of people through campaigns where they contribute money or make donations, often getting something in return for their support.

- Start-up aid, e.g. government loans to help founders build up their start-up capital.

Debt financing

Debt is the other way of financing companies. Unlike equity, debt offers lenders a limited, contractually guaranteed return on their investment.

Your debt collection agency undertakes to pay lenders' interest and repay the capital borrowed according to a pre-agreed schedule. Lenders are therefore making money whether or not your company makes a profit.

As a result, the only risk lenders take is that of your debt collection agency going bankrupt, so they're extremely conservative and will want to see prudent, hands-on management of the company's finances.

From the point of view of the company and all its stakeholders (workforce, customers, suppliers, etc.), the company's contractual obligation to repay lenders increases the risk for all. As a result, there is a certain caution towards companies which are too heavily indebted.

Businesses can borrow debt in two main ways:

- Against assets: this is the most common way of borrowing. The bank funds a percentage of the price of an asset (a vehicle or a building, for example) and takes the asset as collateral. If the business cannot repay the loan, the bank takes the asset and sells it to reduce losses.

- Against cash flows: the bank looks at how much profit and cash flow the business expects to make in the future. Based on these projections, it assigns a credit risk to the business and decides how much the business can borrow and under what terms (amount, interest rate, and duration of the loan).

It's difficult to borrow against future cash flows when you're starting a debt collection agency, because the business doesn't yet have historical data to reassure about the credibility of cash flow forecast.

Borrowing to finance a portion of equipment purchases is therefore often the only option available to founders. The assets that can be financed with this option must also be easy to resell, in the unfortunate event that the bank is forced to seize them, which could limit your options even further.

As far as possible sources of borrowing are concerned, the main ones here are banks and credit institutions. Bear in mind, however, that each institution is different, in terms of the risk it is prepared to accept, what it is willing to finance, and how the risk of your project will be perceived.

In some countries, it is also possible to borrow from private investors (directly or via crowdfunding platforms) or other companies, but not everywhere.

Key points about financing your debt collection agency

Multiple solutions are available to help you raise the initial financing you need to open your debt collection agency. A minimum amount of equity will be needed to give the project credibility, and bank financing can be sought to complete the financing.

Launching your debt collection agency and monitoring progress against your forecast

Once you’ve secured financing, you will finally be ready to launch your debt collection agency. Congratulations!

Celebrate the launch of your business and acknowledge the hard work that brought you here, but remember, this is where the real work begins.

As you know, 50% of business start-ups do not pass the five-year mark. Your priority will be to do everything to secure your business's future.

To do this, it is key to keep an eye on your business plan to ensure that you are on track to achieve your goals.

No one can predict the future with certainty, so it’s likely that your debt collection agency's financial performance will differ from what you predicted in your forecast.

This is why it is recommended to make several forecasts:

- A base case (most likely)

- An optimistic scenario

- And a pessimistic scenario to test the robustness of your financial model

If you follow this approach, your numbers will hopefully be better than your optimistic case and you can consider accelerating your expansion plans. That’s what we wish you anyway!

If, unfortunately, your figures are below your base case (or worse than your pessimistic case), you will need to quickly put in place corrective actions, or consider stopping the activity.

The key, in terms of decision-making, is to regularly compare your real accounting data to your debt collection agency's forecast to:

- Measure the discrepancies and promptly identify where the variances with your base case come from

- Adjust your financial forecast as the year progresses to maintain visibility on future cash flow and cash position

There is nothing worse than waiting for your accountant to prepare your year-end accounts, which can take several months after the end of your financial year (up to nine months in the UK for example), to realise that the performance over the past year was well below the your base case and that your debt collection agency will not have enough cash to keep running over the next twelve months.

This is why using a financial forecasting solution that integrates with accounting software and offers actuals vs. forecast tracking out of the box, like the financial dashboards we offer at The Business Plan Shop, greatly facilitates the task and significantly reduces the risk associated with starting a business.

Need inspiration for your business plan?

Avoid writer's block and draft your own business plan in no time by drawing inspiration from dozens of business plan templates.

Key takeaways

- To open a debt collection agency you need to go through each of the 15 steps we have outlined in this guide.

- The financial forecast is the tool that will enable you to check that your project can be profitable and to estimate the investment and initial financing requirements.

- The business plan is the document that your financial partners will ask you to produce when seeking finance.

- Once you have started trading, it will be essential to keep your financial forecasts up to date in order to maintain visibility of the future cash flow of your debt collection agency.

- Leveraging a financial planning and analysis platform that seamlessly integrates forecasts, business plans, and real-time performance monitoring — like The Business Plan Shop — simplifies the process and mitigates risks associated with launching a business.

We hope this practical guide has given you a better understanding of how to open a debt collection agency. Please do not hesitate to contact our team if you have any questions or if you would like to share your experience of setting up your own business.

Also on The Business Plan Shop

Do you know someone who is thinking about opening a debt collection agency? Share our guide with them!

Founder & CEO at The Business Plan Shop Ltd